{kind=link}

Paying off old collections won’t always raise your credit score.

It depends on which scoring model a lender uses and whether the debt can still be sued.

Some scoring systems ignore paid collections, while older ones treat paid and unpaid the same.

Even if your score doesn’t move, paying can stop lawsuits, end resales, and remove medical collections in many cases.

This post shows when paying is worth it, when to leave a debt alone, and the exact first steps to take so you don’t accidentally restart the legal clock.

Key Guidance on Whether Paying Old Collections Improves Credit

Collection accounts are one of the worst things that can land on your credit report. Payment history makes up about 35–40% of your score, so when an account goes to collections, it tells lenders you didn’t pay what you owed. Your score drops the moment the original account went delinquent, not when some collector bought it.

Will paying off an old collection actually boost your score? Maybe. It depends entirely on which scoring model the lender happens to use when they pull your credit. Some newer models don’t care about paid collections at all. Older ones treat paid and unpaid collections exactly the same. You won’t know which version your bank or credit card company uses, so you’re basically guessing.

But even if your score doesn’t jump right away, paying can still help in other ways. Paid medical collections now get removed from your report completely, thanks to recent reporting changes. Paying also cuts off legal risk, stops the debt from getting resold to yet another agency, and shows future lenders you took care of your mess.

Here’s when paying actually matters and when it doesn’t:

- Paying helps your score if the lender uses a newer model that ignores paid collections or skips certain medical debt.

- Paying changes nothing if the lender uses an older model that counts paid and unpaid collections the same way.

- Paying protects you legally if the account is still within your state’s lawsuit window and you want to avoid garnishment or a judgment.

- Leaving it alone might be smarter if the debt’s really old, the statute of limitations expired, and paying could restart the legal clock.

How Old Collection Accounts Show Up on Your Credit Report

Most creditors send accounts to collections after about 90 days of nonpayment. Once it reaches a collection agency, that agency reports it to Equifax, Experian, and TransUnion. The collection sticks around for seven years from the date of your first missed payment, not from when the collector got involved.

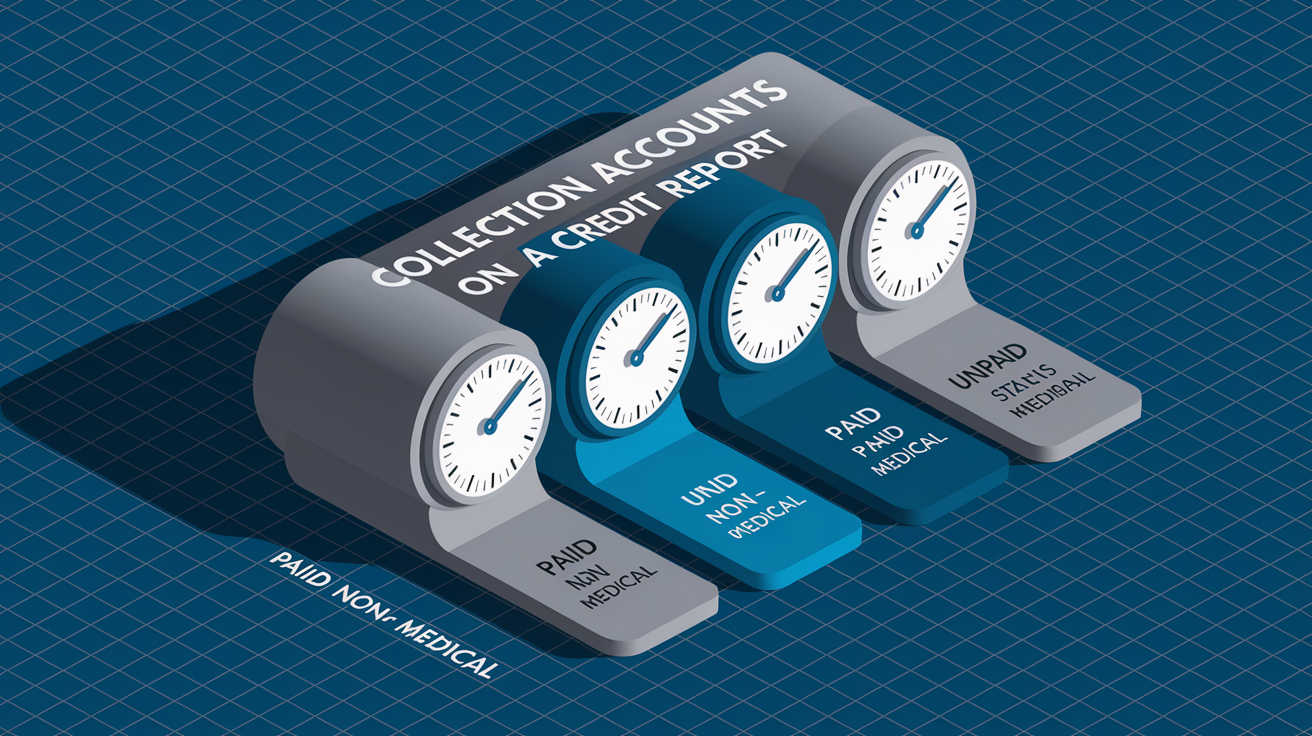

Paying off a collection doesn’t erase it. It stays on your report for the full seven years but switches to a “paid” status. Medical debt is the exception. Paid medical collections don’t get reported anymore, and unpaid medical collections under $500 are also excluded.

| Collection Type | How It Appears on Report | Reporting Duration |

|---|---|---|

| Paid non-medical | Shows as “paid collection” for the full period | 7 years from first delinquency |

| Unpaid non-medical | Shows as “collection account” with outstanding balance | 7 years from first delinquency |

| Paid medical | Removed from report entirely | Not reported |

| Unpaid medical | Appears only if balance is $500 or more | 7 years from first delinquency (if above threshold) |

Credit Score Impact of Paid vs. Unpaid Collection Accounts

How paid collections affect your score comes down to which scoring model the lender uses. Different models treat them completely differently, so paying might help with one lender and do nothing with another. Lenders don’t usually tell you which model they’re pulling, so you’re taking a guess.

The two big scoring systems are FICO and VantageScore, and each one has released multiple versions over the years. Older versions penalize collections harder. Newer ones go easier once you’ve paid.

FICO Model Treatment

FICO Score 8 is super common with credit card companies and auto lenders, and it treats paid and unpaid collections almost the same. If the collection is $100 or more, it hurts your score whether you pay or not. FICO Score 9 and FICO Score 10 ignore paid collections completely and go lighter on unpaid medical collections. If a lender pulls one of those newer models and you’ve paid everything off, those accounts won’t touch your score.

VantageScore Model Treatment

VantageScore 3.0 and 4.0 both ignore paid collections, no matter what kind of debt or how much you owed. They also skip all medical collections, paid or unpaid. If a lender uses VantageScore, paying off a collection stops it from affecting your score. Unpaid non-medical collections still count against you until you pay them off.

Mortgage and Lender Variation

Mortgage lenders have stuck with older FICO models for a long time, especially FICO Score 8 and even earlier versions. That means paying collections might not improve the scores mortgage lenders actually see. In 2022, the federal regulator overseeing conforming mortgages mandated a switch to FICO Score 10 T and VantageScore 4.0. The transition should be done by the end of 2025, and once that happens, more mortgage applicants will catch a break from the newer models that ignore paid collections.

Financial and Legal Risks of Paying Very Old Collection Accounts

Before you pay an old collection, you need to figure out if the debt is still legally enforceable. Every state has a statute of limitations on debt collection, usually three to six years, which sets the clock on how long a collector can sue you. Once that expires, the debt becomes “time-barred,” meaning the collector can’t file a lawsuit to force you to pay.

Paying or even acknowledging a really old debt can restart the statute of limitations in some states. Make a partial payment, sign a written agreement, or confirm the debt is yours, and the clock might reset. Now the collector has a fresh shot at suing you. This is especially risky with “zombie debt,” accounts that have been sold over and over and are almost off your report.

Even if the statute of limitations expired, the collection can still sit on your credit report for the full seven years from when you first missed a payment. Paying won’t make it disappear any faster unless you negotiate a pay-for-delete deal in writing. If the debt’s still within the statute and the collector has threatened to sue, paying or settling is usually safer to avoid a judgment, wage garnishment, or bank account levy.

When Paying Old Collections Might Help Your Credit or Financial Stability

Paying off old collections won’t always boost your score right away, but it can still improve your financial position in ways that matter when you apply for credit. Some lenders review your full credit report manually and care about whether collections have been resolved, even if their scoring model doesn’t reward you for paying. Mortgage underwriters, for instance, might require that all collections above a certain amount be paid before they’ll approve your loan.

Paying collections can also stop ongoing fees and interest charges that some collectors tack on after buying the account. Once you pay, the account can’t be resold to another agency. That cleans up your credit file and cuts down on future collection calls or letters. If you’re planning to apply for a mortgage, auto loan, or certain professional licenses, clearing collections can remove red flags that lenders or licensing boards look for during manual review.

Here’s when paying old collections is likely to help:

- You’re applying for a mortgage and the underwriter won’t close until collections are paid.

- The collection is racking up interest or fees and the balance keeps growing.

- You want to stop collection calls and prevent the debt from being resold again.

- A lender told you they review paid status manually even if it doesn’t change the score they pull.

- The collection is medical debt, which gets removed from your credit report once you pay it.

Negotiation Strategies: Pay-for-Delete, Settlement, and Written Agreements

Before you pay any collection, negotiate the terms in writing. Collection agencies often buy debts for pennies on the dollar, so they’ve got room to accept less than the full balance or agree to remove the account from your credit report in exchange for payment. The two most common strategies are pay-for-delete and settlement offers.

Don’t agree to anything over the phone without written confirmation. Verbal promises from collectors aren’t enforceable. Once you make a payment, your leverage is gone. Request that all agreements be sent to you in writing before you send any money, and keep copies of every document and payment confirmation.

Pay-for-Delete Agreements

A pay-for-delete agreement is when a collection agency agrees to remove the account from your credit report in exchange for full or partial payment. This is the best outcome because it erases the collection once the payment clears. Collectors aren’t legally required to honor pay-for-delete requests, though, and some refuse because credit bureaus discourage it. If a collector agrees, get the promise in writing before you pay, and spell out the exact date the account will be removed from all three bureaus. If they won’t provide written confirmation, assume they won’t follow through.

Settlement and Reduced-Balance Options

If a collector won’t agree to deletion, you can often settle for less than the full balance. Many agencies will take 30% to 60% of the original amount, especially if the debt’s several years old. When you settle, the account will show up on your credit report as “settled” instead of “paid in full,” which some lenders view a little less favorably. Always negotiate the settlement amount and confirm in writing whether the account will be reported as “paid” or “settled” before sending payment. If you can afford to pay in full and the collector won’t agree to deletion, paying in full usually looks better than settling.

Alternatives to Paying Old Collections

Paying isn’t always the best or only option for dealing with old collections. If the debt is wrong, you can dispute it with the credit bureaus and have it removed. If the collection is accurate but happened because of a one-time hardship, you can ask the original creditor to remove it as a goodwill gesture. And if the debt’s close to falling off your credit report naturally, waiting might be the easiest move.

Disputing a collection only works if the information is incorrect or the collector can’t verify the debt. When you file a dispute with Equifax, Experian, or TransUnion, the bureau has to investigate within 30 days. If the collection agency can’t provide proof that the debt is valid and yours, the bureau has to remove it. Accurate collections can’t be removed through disputes, though, and filing the same dispute over and over won’t work.

| Alternative | When It Works | Risks |

|---|---|---|

| Dispute the account | When the debt isn’t yours, the balance is wrong, or the collector can’t verify | Only removes inaccurate items; accurate collections stay |

| Send a goodwill letter | When the debt was caused by a one-time hardship and you have a strong payment history otherwise | No guarantee of success; original creditor may ignore the request |

| Request debt validation | Within 30 days of first contact from collector to force proof of debt | Collector may provide proof, and then collection continues |

| Wait for the 7-year mark | When the collection is close to expiring and statute of limitations has passed | Collection remains on report and may still affect scores until it expires |

How to Prioritize Debt Payments When You Have Multiple Collection Accounts

If you’ve got multiple old collections and limited money to pay them, you need a plan to figure out which ones to tackle first. Paying randomly or based on whichever collector is bugging you the most is rarely the smart move. Prioritize based on legal risk, credit impact, and financial stability.

Start by checking the statute of limitations for each debt in your state. If a collection is still within the legal window and the collector has threatened a lawsuit, that one should be your top priority to avoid wage garnishment or a court judgment. Next, figure out which accounts are most likely to be reviewed manually by lenders, like collections above $500 or accounts with the original creditor instead of some third-party agency. And make sure you’re not draining your budget or emergency savings just to pay old debts.

Here’s a simple way to prioritize paying multiple collections:

- Check the statute of limitations for each debt and focus on any account that’s still legally collectible.

- Figure out which collectors are actively chasing the debt and which accounts are sitting there doing nothing.

- Decide which collections are most likely to affect loan approvals based on the type of lender and loan you’re going for.

- Negotiate settlements or pay-for-delete agreements in writing before making any payments.

- Pay off smaller balances first if you want quick wins to reduce the number of open collections (debt snowball method).

- Pay off the highest-interest or highest-balance accounts first if you want to cut your total cost (debt avalanche method).

Steps to Rebuild Credit After Addressing Collection Accounts

Once you’ve paid, settled, or disputed your collections, the next step is rebuilding your credit by establishing a consistent pattern of on-time payments and responsible credit use. Paying off collections removes a big obstacle, but it won’t automatically raise your score back to where it was before everything went sideways. Recovery takes time, and the fastest way to speed it up is to focus on the factors that matter most to scoring models.

The single most important thing you can do is pay every bill on time moving forward. Payment history is the biggest factor in your credit score. Even one missed payment can set you back. Set up automatic payments for at least the minimum due on all credit cards and loans, and use calendar reminders for bills that can’t be automated. If you don’t have any active credit accounts, think about opening a secured credit card. It requires a cash deposit and reports to all three bureaus just like a regular card.

Keep your credit card balances below 30% of your total credit limit. Ideally below 10%. Credit utilization, the ratio of your balances to your limits, is the second-biggest scoring factor after payment history. Don’t apply for new credit unless you really need it, since each application triggers a hard inquiry that can knock a few points off your score for up to 12 months. Monitor your credit reports regularly using the free annual reports from each bureau to confirm paid collections are accurately reported and to catch any new errors early.

Here are five specific ways to rebuild credit after collections:

- Open a secured credit card and use it for small recurring purchases, paying the full balance each month.

- Consider a credit-builder loan, which holds your loan amount in a savings account and releases it once you’ve made all payments.

- Become an authorized user on a family member’s credit card with a long, positive payment history (make sure the account reports to all three bureaus).

- Cut credit utilization by paying down existing balances or requesting credit limit increases on cards in good standing.

- Avoid new credit applications for at least six months after paying collections to let your score stabilize and reduce hard inquiries.

Final Words

You now know how collection accounts show up, why they act as derogatory marks, and that paying them may or may not change your score depending on how models treat paid collections.

Simple decision rule: if you need better lender outcomes or are prepping for a mortgage, try to negotiate a written deal and consider paying. If the debt is very old or near the statute of limitations, verify dates and explore disputes or goodwill letters first.

If you’re still asking should you pay off old collections to improve credit, pull your reports, check first-delinquency dates, and pick the option that lowers your risk. You can make steady progress.

FAQ

Q: Will my credit score improve if I pay off collections, and is it worth paying off old collection accounts?

A: Paying off collections may or may not improve your credit score, and it can still be worth it. Some scoring models ignore paid collections; paying stops collection activity and improves lender perception.

Q: What is the 7 7 7 rule in collections?

A: The 7 7 7 rule in collections isn’t a legal standard; the key timeline is seven years from the first delinquency for reporting, though practices and exceptions can vary by situation.

Q: What is the biggest killer of credit scores?

A: The biggest killer of credit scores is poor payment history, meaning late, missed, or defaulted payments. Payment history matters most; even one severe late mark can cause a major drop.