{kind=link}

Merging student loans and credit cards into one payment sounds smart, but it’s not as simple as it looks.

If you have federal student loans, federal consolidation programs won’t let you mix in credit card debt.

You can combine both with a private product like a personal consolidation loan, a balance transfer card, or private refinancing, but that usually means giving up federal protections (income-driven plans, forgiveness, deferment).

This article shows when combining makes sense, the trade-offs, and a simple rule: keep federal loans federal unless you’re sure the private deal is clearly better.

Understanding Whether Student Loans and Credit Cards Can Be Combined Into One Payment

Federal consolidation programs won’t let you merge student loans and credit cards into one payment. Direct Consolidation Loans only work with eligible federal student loans. Credit cards are unsecured consumer debt, and the federal system treats them as completely separate.

If you want both debts under one monthly payment, you’ll need a private product. Personal debt consolidation loans are the most common route. These unsecured loans pay off your student loans and credit card balances, leaving you with just one new loan. Balance transfer credit cards can handle credit card debt and sometimes small student loan amounts, but they rarely cover full student loan balances and the promotional period usually only lasts about 12 months.

Combining debts this way carries real risks if you currently hold federal student loans. When you use a personal loan or private refinancing to pay off federal loans, you permanently lose federal protections. Income driven repayment plans, Public Service Loan Forgiveness eligibility, deferment, and forbearance programs all disappear. If your financial situation changes or you work in public service, those protections can be worth much more than a slightly lower interest rate.

How Debt Consolidation Works for Student Loans vs. Credit Cards

Debt consolidation for student loans and credit cards follows completely different processes because the debts are classified differently. Federal student loan consolidation uses a Direct Consolidation Loan that combines multiple federal loans into one new federal loan with a single servicer. The new interest rate is the weighted average of your existing federal loan rates, rounded up to the nearest one eighth of one percent. Federal consolidation doesn’t reduce your interest rate. It just creates one payment and preserves your access to federal repayment options like income driven plans and forgiveness programs.

Credit card debt consolidation typically happens through a personal loan or a balance transfer credit card. A personal loan pays off your credit cards in full and replaces them with one installment loan, usually with a fixed interest rate and a repayment term between two and seven years. Balance transfers move credit card balances onto a new card, often with a 0% introductory APR that lasts 12 to 21 months, but you’ll pay a transfer fee of 3% to 5% of the balance. Private student loan refinancing works differently from federal consolidation. It replaces your existing loans with a new private loan that may offer a lower APR if you have strong credit and income, but it requires a credit check and can include both private and federal student loans.

Here are the key differences between consolidating student loans and consolidating credit cards:

Debt type classification: Federal student loans remain federal loans when consolidated through Direct Consolidation. Credit cards and private student loans must be refinanced or consolidated through private lenders.

Eligibility: Federal consolidation requires loans in repayment or grace period and no half time enrollment. Credit card and private loan consolidation depends on your credit score, income, and debt to income ratio.

Interest rate rules: Federal consolidation creates a weighted average rate with no reduction. Private refinancing and personal loans offer rates from roughly 6% to 36% based on credit.

Credit score requirements: Federal consolidation doesn’t check credit. Private consolidation and balance transfers generally require scores of 670 or higher for the best rates.

Repayment terms: Federal consolidation offers 10 to 30 years. Private lenders commonly offer 5 to 25 years for refinancing and 2 to 7 years for personal loans.

Protections lost or preserved: Federal consolidation keeps income driven repayment, PSLF, and forbearance. Private refinancing or personal loans eliminate all federal protections if used to pay off federal loans.

Options That Can Bring Both Student Loans and Credit Cards Into One Payment

A personal debt consolidation loan is the most straightforward way to combine student loans and credit cards into one monthly payment. These unsecured loans typically start at a minimum of $5,000, and the average personal loan funded in 2023 was about $33,000. You can use the loan to pay off both your student loan servicer and your credit card issuers, leaving you with just one lender and one fixed monthly payment. Interest rates range from roughly 6% to 36% depending on your credit score and income, so the blended rate might be lower than your credit cards but higher than your student loans. You’ll also pay an origination fee of 0% to 5% with many lenders, and the loan term is usually two to seven years.

Balance transfer credit cards can be helpful if you have smaller debt amounts and strong enough credit to qualify for a 0% promotional APR. These offers typically last 12 to 21 months, and you’ll pay a transfer fee of 3% to 5% of the amount you move onto the card. The 0% window can save significant interest if you pay off the full balance before the promotional period ends, but transferring a large student loan balance is often impractical because most people can’t pay off tens of thousands of dollars within a year. Balance transfers work best for smaller credit card balances or modest private student loan amounts when paired with an aggressive payoff plan.

Home equity loans and home equity lines of credit (HELOCs) can also combine debts, offering rates in the mid single to low double digits, often around 5% to 8% depending on market conditions and your credit. These products use your home as collateral, which means lower rates but higher risk. If you fall behind on payments, you could lose your house. Debt Management Plans through nonprofit credit counseling agencies are another option. They bundle your credit card debts into one monthly payment with reduced interest rates negotiated by the agency, but many DMPs won’t include federal student loans or will handle them separately.

Here are five key points about combining debts with a personal loan:

Lower your overall interest rate if credit card APRs are high and you qualify for a competitive personal loan rate based on strong credit.

Lose all federal student loan protections if you use the personal loan to pay off federal loans. No more income driven repayment or forgiveness.

Simplify budgeting and bill tracking with a single fixed monthly payment instead of juggling multiple due dates and servicers.

Pay origination fees and possibly prepayment penalties, depending on the lender’s terms.

Potentially increase total interest paid if you extend the repayment term beyond what you currently owe.

Pros and Cons of Combining Credit Cards and Student Loans Together

Combining student loans and credit cards into one payment can make your monthly budget simpler and more predictable, especially if you’re managing multiple due dates and servicers. One fixed monthly payment is easier to track than separate payments to federal loan servicers, private lenders, and multiple credit card companies. If you qualify for a personal loan with an interest rate that falls between your low student loan rate and your high credit card rate, you may reduce the blended cost of borrowing and potentially save on interest compared to paying only minimum payments on high APR credit cards.

The major risks come from longer repayment terms and the permanent loss of federal benefits. Extending your repayment period lowers your monthly payment but can add thousands of dollars in total interest over the life of the loan. Refinancing federal student loans into a private product eliminates income driven repayment plans, Public Service Loan Forgiveness, deferment, and forbearance. Protections that can be critical if your income drops or you work in public service. Hard credit inquiries and the opening of a new account may temporarily lower your credit score by fewer than 5 points, but paying off credit card balances will reduce your credit utilization, which can improve your score over time if you keep those cards open and avoid new balances.

| Benefit or Risk | Explanation |

|---|---|

| Lower monthly payment | Extending the term to 7 or more years reduces the amount you owe each month, freeing up cash flow for other expenses. |

| Simplified payment structure | One monthly payment to one lender instead of juggling federal servicers, private lenders, and multiple credit card companies. |

| Loss of federal protections | Using a private loan to pay off federal student loans eliminates income driven repayment, PSLF eligibility, deferment, and forbearance. |

| Higher total interest cost | Longer repayment terms mean more interest accrues over time, potentially costing thousands more than the original repayment schedule. |

| Credit score effects | Hard inquiry and new account may lower score short term. Paying off credit cards reduces utilization and can boost score long term. |

| Fees | Origination fees of 0% to 5% on personal loans and 3% to 5% transfer fees on balance transfer cards add upfront costs. |

Eligibility Requirements and Credit Score Considerations for Consolidation and Refinancing

Private lenders that offer personal loans or student loan refinancing typically require a credit score of at least 670 to qualify for competitive rates, and the best offers, including 0% balance transfer cards, often go to applicants with scores of 700 or higher. If your score is below that range, you may still qualify but will pay a higher interest rate, which can reduce or eliminate the benefit of consolidating. Lenders also check your income and employment history to confirm you can afford the new monthly payment, and they calculate your debt to income ratio by dividing your total monthly debt payments by your gross monthly income. Most lenders prefer a DTI below 40% to 50%, though exact thresholds vary.

If you don’t meet credit or income requirements on your own, adding a cosigner with strong credit and stable income can expand your eligibility and may lower the interest rate you’re offered. A cosigner agrees to repay the loan if you can’t, so lenders view the application as less risky. Some private lenders offer cosigner release programs that allow you to remove the cosigner after you make a certain number of on time payments, but not all lenders provide that option.

Applying for a personal loan or refinancing triggers a hard credit inquiry, which may reduce your credit score by fewer than 5 points temporarily. The score impact is usually small and fades within a few months if you continue making on time payments. Opening a new loan account also lowers the average age of your credit accounts, which can affect your credit history length, but the long term effect depends on how you manage the new account and whether you keep your old credit card accounts open after paying them off.

Step by Step Process for Consolidating Student Loans and Credit Cards Using a Personal Loan

Using a personal loan to combine your student loans and credit cards into one payment requires careful planning and documentation, but the process is straightforward if you follow each step in order. Start by gathering your current balances, interest rates, and monthly payments for every debt you want to consolidate so you know exactly how much you need to borrow and can compare the new loan terms against what you’re paying now.

Calculate your total debt and monthly obligations. Add up all student loan and credit card balances. Note the interest rate and minimum payment for each account so you can compare the total cost and monthly payment of a new loan.

Check your credit score and review your credit report. Know where you stand before applying. Scores of 670 or higher generally qualify for better rates, and you can dispute any errors on your report that might hurt your approval odds.

Shop and compare lenders using prequalification. Most online lenders offer prequalification with a soft credit check that won’t affect your score. Compare APRs, terms, fees, and whether the lender allows you to pay off student loans and credit cards with the same loan.

Choose the loan with the best combination of rate and term. Pick the shortest repayment period you can afford to minimize total interest, and confirm there are no prepayment penalties if you want to pay extra or pay off the loan early.

Submit a full application and provide required documents. Lenders typically ask for recent pay stubs, W-2 or tax returns, a photo ID, and payoff statements from your current student loan servicers and credit card issuers.

Wait for approval and funding. Processing times vary from a few business days to about 30 days depending on the lender and how quickly you submit documents. Some lenders fund within one to three business days after approval.

Use the loan proceeds to pay off your student loans and credit cards. Most lenders either send funds directly to your creditors or deposit the money in your bank account for you to distribute. Continue making payments on your old accounts until you confirm the balances are zero to avoid late fees or credit damage.

Alternatives to Consolidating Student Loans and Credit Cards

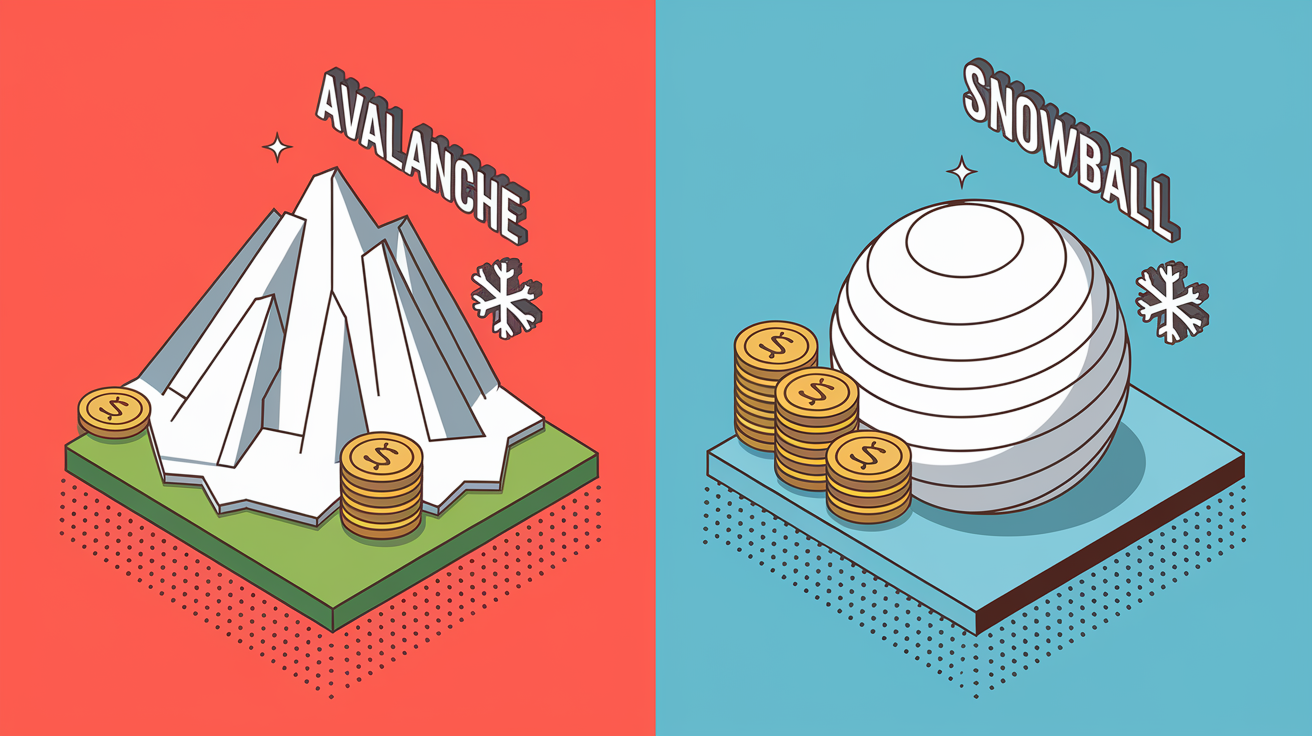

If combining your student loans and credit cards into one payment isn’t the right fit, or if you want to avoid losing federal protections, you can use targeted repayment strategies to manage both debts without consolidation. The debt avalanche method prioritizes paying extra money toward the debt with the highest interest rate while making minimum payments on everything else. For example, if your credit cards charge 20% and your student loans charge 6%, you’d focus extra payments on the credit cards first to eliminate the most expensive debt faster. This approach saves the most money in total interest.

The debt snowball method works in reverse. You pay off the smallest balance first, regardless of interest rate, then roll that payment into the next smallest debt. This method can build momentum and motivation because you see accounts disappear quickly, even if it costs slightly more in interest than the avalanche approach. Even small extra payments make a measurable difference. Paying an extra $25 per month on a high interest debt can shorten your payoff timeline by months and reduce the total interest you pay by hundreds of dollars.

Here are five alternatives to formal consolidation:

Debt avalanche: Focus extra payments on the highest interest debt first to minimize total interest cost.

Debt snowball: Pay off the smallest balance first to build quick wins and motivation.

Extra monthly payments: Add even $25 or $50 to one debt each month to accelerate payoff and reduce interest.

Debt Management Plan through credit counseling: Nonprofit agencies negotiate lower interest rates on credit cards and create one monthly payment, though most DMPs don’t include federal student loans.

Refinance student loans separately: Keep credit cards on their own repayment plan and refinance only student loans if you can get a lower rate without losing federal benefits you actually need.

Long Term Financial Impact of Combining Student Loans and Credit Cards

Combining student loans and credit cards into one payment can reshape your monthly budget and long term financial trajectory in ways that aren’t obvious at first. Lowering your monthly payment by extending the repayment term to seven, ten, or even fifteen years frees up cash flow for other goals like building an emergency fund or saving for a down payment, but it also increases the total amount of interest you’ll pay over the life of the loan, sometimes by several thousand dollars. If your current debts would be paid off in five years and you stretch the new loan to ten, you’re paying interest for twice as long, even if the rate is lower.

The loss of federal student loan benefits has financial consequences that can compound over decades. Income driven repayment plans can lower or even pause your monthly payments if your income drops due to job loss, a career change, or family circumstances. Public Service Loan Forgiveness can erase your remaining federal loan balance after ten years of qualifying payments if you work for a government or nonprofit employer. Deferment and forbearance options provide breathing room during financial emergencies without damaging your credit. Once you refinance federal loans into a private product, those safety nets disappear permanently, and you’re left with a fixed monthly obligation that doesn’t adjust to your circumstances.

Your credit score and overall debt load also shift when you consolidate. Paying off credit card balances reduces your credit utilization ratio, which can boost your score, but opening a new loan account lowers the average age of your credit and may hurt your score short term. If you keep your credit cards open after paying them off and avoid running up new balances, you’ll maintain a healthier credit profile long term and preserve access to credit for true emergencies.

Frequently Asked Questions About Combining Student Loans and Credit Cards

Can federal Direct Consolidation Loans include credit card debt?

No. Federal Direct Consolidation Loans can only combine eligible federal student loans and can’t include credit cards, private student loans, or any other type of consumer debt.

Will consolidating my debts close my credit card accounts?

No. Using a personal loan or balance transfer to pay off credit card balances doesn’t automatically close those accounts. The cards remain open unless you choose to close them, and keeping them open can help your credit utilization ratio.

Does refinancing federal student loans into a private consolidation loan affect forgiveness eligibility?

Yes. Refinancing federal student loans with a private lender permanently removes your eligibility for Public Service Loan Forgiveness, income driven repayment plans, and other federal forgiveness programs.

How does consolidating student loans and credit cards affect my credit score?

Consolidation typically causes a small, temporary drop due to the hard credit inquiry and the new account, but paying off credit card balances lowers your credit utilization, which can improve your score over time if you make on time payments on the new loan.

Can I use a Debt Management Plan to combine student loans and credit cards?

Most Debt Management Plans offered by nonprofit credit counseling agencies focus on unsecured debts like credit cards and may include private student loans, but they typically don’t include federal student loans unless you arrange separate handling or the agency offers a specialized program.

Final Words

in the action, we explained that federal Direct Consolidation only covers federal student loans and can’t include credit cards. We reviewed private refinancing, personal loans, balance transfers, and the main risk: losing federal protections like income-driven plans and forgiveness.

If you’re deciding, a simple rule helps: keep federal loans in federal programs unless private savings clearly beat lost benefits. Compare rates, prequalify, and get payoff quotes.

If your question is can you consolidate student loans and credit cards, the short answer is yes, but only with private products and real trade-offs. Start by checking balances and prequalifying.

FAQ

Q: Can I consolidate my student loans and credit cards together?

A: You generally can’t consolidate federal student loans and credit cards together through federal programs; you can combine both with a private personal loan or refinancing, but you may lose federal protections and face higher costs.

Q: How much would a $30,000 student loan be monthly?

A: A $30,000 student loan monthly payment depends on rate and term. Examples: 5% for 10 years ≈ $319/month; 6% for 20 years ≈ $215/month; 8% for 5 years ≈ $610/month.

Q: Why does Dave Ramsey say not to consolidate debt?

A: Dave Ramsey says not to consolidate debt because it can extend repayment, increase total interest, and hide progress. He prefers the debt snowball, paying smallest balances first to build momentum and stay focused.

Q: How to pay off $30,000 in debt in 1 year?

A: To pay off $30,000 in one year you need about $2,500 monthly plus interest; cut spending, boost income (side gigs), use windfalls, consider low-rate loans or balance transfers, and track payments weekly.