{kind=link}

Think one account can’t beat taxes three ways?

Think again.

A Health Savings Account (HSA) gives a triple tax advantage: pre-tax or deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

This post explains exactly how each leg works, who qualifies, and the simple moves that make the biggest difference.

If your employer offers a high-deductible plan, start by contributing enough to get any employer deposit.

No jargon, just clear steps so you can save on taxes now and later.

Understanding the HSA Triple Tax Advantage in Clear Terms

A Health Savings Account (HSA) is a tax sheltered savings account you can use alongside a qualified High Deductible Health Plan (HDHP). The triple tax advantage means you get a tax break at three different points: when money goes in, while it grows, and when you pull it out for medical expenses.

The first advantage is tax deductible contributions. When you contribute through payroll, the money comes out before federal income tax and payroll taxes get calculated. If you contribute on your own outside of payroll, you take an above the line deduction on your tax return. Employer contributions count toward your annual limit and don’t show up as taxable income. The second advantage is tax free growth. Any interest, dividends, or capital gains your HSA earns inside the account aren’t taxed while they accumulate. The third advantage is tax free withdrawals for qualified medical expenses, which the IRS defines in Publication 502. This includes doctor visits, prescriptions, dental care, vision expenses, preventive care, copayments, deductibles, and coinsurance.

Here’s how the numbers work. Say you contribute $4,150 (the 2024 individual limit) and you’re in the 24% federal tax bracket. That contribution reduces your federal tax bill by $996. If the contribution also reduces your payroll tax exposure at 7.65%, you save an additional $317 in payroll taxes. Your total federal and payroll tax savings is roughly $1,313 in the year you contribute.

Contribution tax savings: Pre tax payroll contributions reduce both federal income tax and payroll taxes. Direct contributions reduce federal income tax via an above the line deduction.

Growth tax savings: Earnings inside the HSA (interest, dividends, capital gains) grow completely tax free with no annual tax reporting required.

Withdrawal tax savings: Distributions used for IRS qualified medical expenses are entirely tax free at any age.

Qualified expense examples: Doctor and specialist visits, prescription medications, dental cleanings and procedures, vision exams and corrective lenses, preventive care screenings.

Real world impact: A $4,150 contribution at 24% federal and 7.65% payroll rates saves approximately $1,313 in combined taxes the year you contribute.

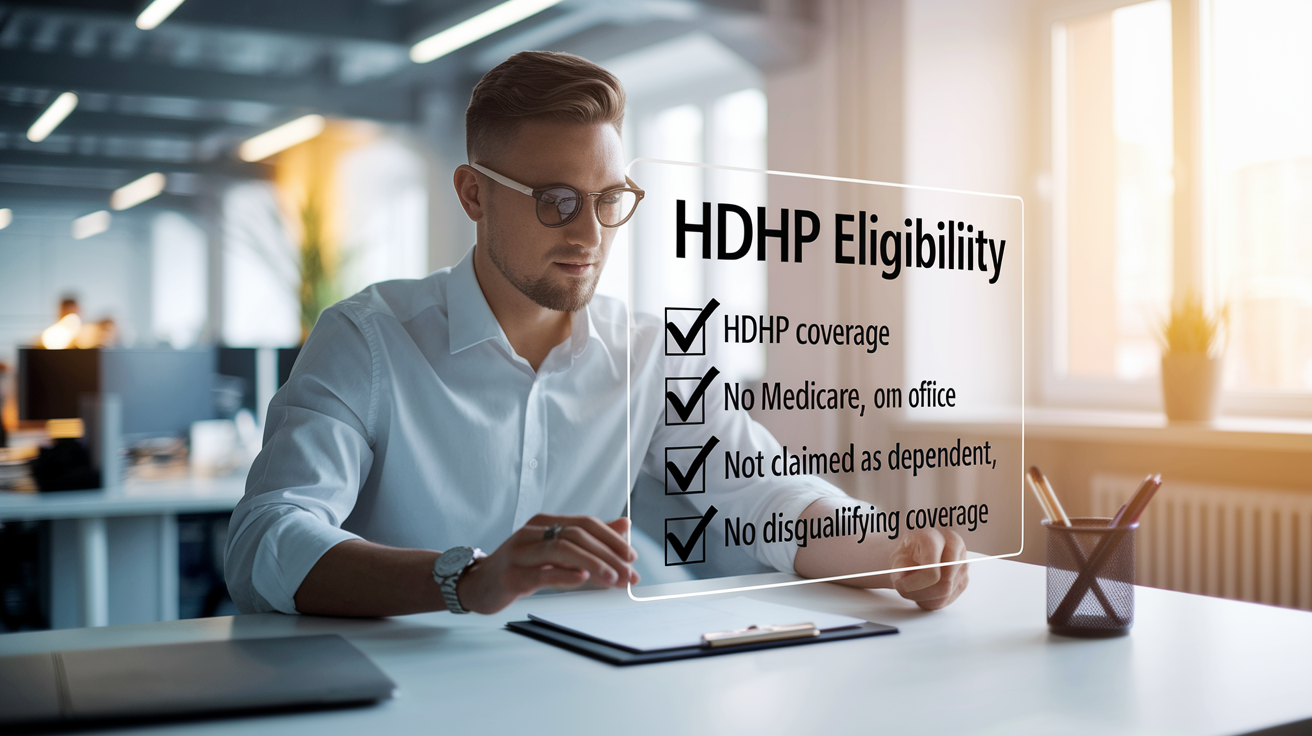

HSA Eligibility Requirements and HDHP Rules Supporting the Triple Tax Advantage

To open and contribute to an HSA, you’ve got to meet specific eligibility rules tied to your health insurance coverage and other factors. The core requirement is enrollment in a High Deductible Health Plan that meets IRS minimum thresholds for deductibles and out of pocket maximums.

For 2024, an HDHP must have a minimum annual deductible of $1,600 for self only coverage or $3,200 for family coverage. The plan’s out of pocket maximum can’t exceed $8,050 for self only or $16,100 for family coverage. Beyond the HDHP requirement, you can’t be enrolled in Medicare, you can’t be claimed as a dependent on someone else’s tax return, and you can’t have other disqualifying health coverage such as a general purpose Health FSA or certain types of spouse or secondary insurance. Once you enroll in Medicare (which can happen automatically at age 65 if you’re receiving Social Security) your HSA contribution eligibility ends immediately, even if you keep working.

You must be covered under an IRS qualified High Deductible Health Plan (HDHP).

You can’t be enrolled in Medicare Part A or Part B.

You can’t be claimed as a dependent on another person’s tax return.

You can’t have disqualifying secondary coverage, including general purpose Health FSAs, Medicaid (in most cases), or certain spouse plan features that cover expenses before the HDHP deductible is met.

Contribution Limits and How They Affect HSA Tax Advantages

The IRS sets annual contribution limits that cap how much you and your employer combined can deposit into your HSA each year. For 2024, the limit is $4,150 for individuals with self only HDHP coverage and $8,300 for those with family coverage. These limits increased from $3,850 and $7,750 respectively in 2023.

If you’re age 55 or older by the end of the tax year, you can make an additional $1,000 catch up contribution on top of the standard limit. Employer contributions (whether direct deposits, matching programs, or seed money) count toward your annual maximum. You have until the tax filing deadline to make contributions for a given tax year. For example, you can contribute for the 2024 tax year until April 15, 2025, as long as you were HSA eligible during 2024. Exceeding the annual limit triggers a 6% excise tax on the excess amount for each year it remains in the account.

2024 contribution limits: $4,150 for self only coverage, $8,300 for family coverage.

2023 contribution limits (for comparison): $3,850 self only, $7,750 family.

Catch up contributions: An additional $1,000 per year if you turn 55 or older during the tax year.

Employer contributions: Any amount your employer deposits counts toward your annual limit.

Contribution deadline: Tax filing deadline of the following year (typically April 15), giving you extra months to maximize contributions and tax savings.

How Tax-Free Growth Inside an HSA Maximizes Long-Term Benefits

Unlike a typical checking or savings account where you pay tax on interest each year, every dollar your HSA earns through interest, dividends, or investment gains grows without any tax reporting or tax drag. This tax free compounding is the second leg of the triple advantage and becomes powerful over long time horizons.

Most HSA custodians offer investment options once your cash balance reaches a minimum threshold, often $1,000 to $2,000. Investment choices vary by provider but typically include mutual funds, index funds, ETFs, and sometimes individual stocks or bonds. Because there are no required minimum distributions, you can let your HSA grow indefinitely, even past age 72 when traditional IRAs force withdrawals.

The compounding effect is significant. If you contribute $4,150 at the start of each year, earn an average annual return of 6%, and repeat this for 20 years, your HSA balance would grow to approximately $153,000. That entire balance (contributions and all growth) can be withdrawn completely tax free if used for qualified medical expenses. Compare that to a taxable brokerage account where you’d owe tax on dividends each year and capital gains tax when you sell, and the HSA’s advantage is clear.

Year 1: Contribute $4,150, ending balance around $4,399 (with 6% growth).

Year 10: Total contributions $41,500, ending balance around $57,000 (growth compounds tax free).

Year 20: Total contributions $83,000, ending balance around $153,000 (all tax free for medical expenses).

Tax-Free Withdrawals and What Counts as Qualified Medical Expenses

Distributions from your HSA are completely free from federal income tax when you use them to pay for expenses the IRS defines as qualified medical expenses in Publication 502. This third tax benefit is what separates HSAs from most other tax advantaged accounts.

Qualified expenses cover a wide range of healthcare costs. Payments to doctors, dentists, and other medical practitioners. Prescription medications and insulin. Hospital services and surgeries. Diagnostic tests and lab work. Mental health counseling and therapy. Chiropractic care. Eyeglasses, contact lenses, and vision exams. Hearing aids. Preventive care such as annual physicals and screenings. Medical equipment like crutches or blood pressure monitors. And costs like copayments, deductibles, and coinsurance under your health plan. The IRS list is long and includes many items people don’t initially think of as “medical,” such as acupuncture, smoking cessation programs, and certain weight loss programs when prescribed by a doctor. You must keep receipts and documentation to prove any withdrawal was for a qualified expense, because the IRS can request substantiation during an audit.

Payments to physicians, surgeons, specialists, and other licensed medical practitioners.

Prescription drugs, over the counter medications with a prescription, and insulin (available without a prescription).

Dental care including cleanings, fillings, crowns, braces, and dentures.

Vision care such as eye exams, prescription glasses, contact lenses, and corrective eye surgery.

Mental health services including therapy, counseling, and psychiatric care.

Health insurance deductibles, copayments, and coinsurance amounts you pay out of pocket.

Penalties, Non-Qualified Withdrawals, and Age-65 Rule Changes

If you withdraw HSA money for something other than a qualified medical expense before you turn 65, you face two hits: ordinary income tax on the full amount plus an additional 20% penalty. This double penalty makes non medical withdrawals expensive and discourages using your HSA as a general savings account.

After you reach age 65, the rules change. Non qualified withdrawals are still subject to ordinary income tax, but the 20% penalty disappears. This makes the HSA function similarly to a traditional IRA for non medical spending after 65. You pay income tax on withdrawals, but there’s no extra penalty. Medical withdrawals remain completely tax free at any age as long as the expense is IRS qualified and you keep proper records.

Before age 65, non qualified withdrawal: A $1,000 distribution for a vacation incurs $240 in federal income tax (24% bracket) plus a $200 penalty (20% of $1,000), leaving you with $560 after taxes and penalties.

After age 65, non qualified withdrawal: The same $1,000 withdrawal incurs only the $240 income tax, with no penalty. You net $760.

Medical withdrawals at any age: A $1,000 distribution for a qualified medical expense incurs zero tax and zero penalty, giving you the full $1,000 benefit.

| Account Type | Contribution Tax Treatment | Withdrawal Tax Treatment |

|---|---|---|

| HSA | Pre-tax or tax-deductible; reduces income and payroll taxes | Tax-free for qualified medical expenses; taxed as income (no penalty after 65) for non-medical |

| Health FSA | Pre-tax via payroll | Tax-free for qualified medical expenses; funds typically forfeited if unused by plan year-end |

| Traditional IRA / 401(k) | Pre-tax or tax-deductible | Fully taxable as ordinary income; 10% penalty if withdrawn before age 59½ (with exceptions) |

| Roth IRA | After-tax (no deduction) | Tax-free if account is 5+ years old and you are 59½ or older |

Comparing HSAs to FSAs, IRAs, and 401(k)s for Tax Efficiency

HSAs occupy a unique space in the tax advantaged account landscape because they combine features from health accounts and retirement accounts. Unlike Health Flexible Spending Accounts (FSAs), HSAs are fully portable. You own the account and it moves with you when you change jobs. FSAs are typically tied to your employer, subject to annual forfeiture rules (use it or lose it), and offer lower contribution limits. HSAs roll over indefinitely with no expiration or forfeiture, letting you build a substantial balance over many years.

When compared to retirement accounts, HSAs offer something neither traditional nor Roth IRAs can match: triple tax benefits. Traditional IRAs and 401(k)s give you a tax deduction on contributions, but every dollar you withdraw in retirement is taxed as ordinary income. Roth IRAs flip that. You contribute after tax dollars, but qualified withdrawals are tax free. HSAs give you both the upfront deduction and the tax free withdrawal, plus tax free growth in between, as long as you use the money for medical expenses. After age 65, an HSA effectively becomes a traditional IRA for non medical withdrawals (taxed as income, no penalty), but it retains the tax free medical withdrawal option forever. No other account structure delivers all three tax advantages in one vehicle.

Strategic Ways to Maximize the Triple Tax Advantage

The most common HSA mistake is treating it like a short term medical checking account. To unlock the full triple advantage, consider paying current medical bills out of pocket when you can afford it, leaving your HSA contributions invested for long term growth. You can reimburse yourself years or even decades later as long as you keep receipts proving the expense was qualified and incurred after your HSA was established. This strategy lets your account compound tax free while you build a large reserve for future healthcare costs or retirement medical expenses.

Timing matters. If you’re approaching age 65, plan your final HSA contributions carefully. Once you enroll in Medicare (which can happen automatically if you’re receiving Social Security benefits) you lose the ability to contribute, even if you’re still working. Some people delay Social Security and Medicare enrollment past 65 to keep contributing to an HSA. Employer contributions are free money, so if your employer offers HSA matching or seed funding, contribute at least enough to capture the full match. Track every qualified expense and keep organized records, because the IRS can request proof of qualified use years after a withdrawal.

HSAs are flexible. You can adjust contributions throughout the year, unlike many retirement plans with fixed deferrals. If your medical costs spike mid year, you can increase contributions to cover them tax free. If costs stay low, you can invest more aggressively and build long term wealth. The key is understanding that the triple tax advantage grows more valuable the longer your money stays in the account and the more it compounds.

Pay small medical bills out of pocket and let your HSA balance grow invested for years or decades. Reimburse yourself later using saved receipts to access tax free cash when you need it most.

Maximize contributions early in the year to give your investments the longest possible time to compound tax free. Front loading contributions beats spreading them across 12 months when markets trend upward.

Capture employer HSA contributions by contributing at least enough to receive any available employer match or seed money. This is immediate, tax free return on your contribution.

Keep meticulous records of every qualified medical expense, including receipts, explanations of benefits, and dates of service, so you can substantiate tax free withdrawals even years later.

Plan Medicare enrollment timing if you’re still working past 65. Delaying Medicare enrollment (when allowed) extends your HSA contribution eligibility and maximizes your total lifetime tax free savings potential.

Final Words

In the action, we explained how HSAs cut taxable income, grow tax-free, and pay out tax-free for qualified medical costs. You also got eligibility rules, 2024 limits, investment growth examples, common qualified expenses, penalties, and practical strategies.

If you have an HDHP and can save, prioritize HSA contributions: cover a deductible, save receipts, and invest what’s extra.

Remember the triple tax advantage of hsa explained here: deductible contributions, tax-free growth, and tax-free medical withdrawals. Start small, be consistent, and you’ll build useful savings.

FAQ

Q: Why does HSA have triple tax advantage?

A: The HSA has a triple tax advantage because contributions cut taxable income (pre-tax or payroll), investments grow tax-free, and withdrawals for IRS-qualified medical expenses are tax-free; a $4,150 contribution at 24% saves about $1,313.

Q: What does Dave Ramsey say about HSA?

A: Dave Ramsey says HSAs can be smart if you can handle a high-deductible plan and treat the HSA like long-term medical savings; he recommends an emergency fund first and avoiding early withdrawals.

Q: Can you use HSA for pet surgery?

A: You cannot use an HSA for pet surgery; HSAs pay for IRS-qualified medical expenses for you, your spouse, and dependents only. Using HSA money for pets triggers taxable, potentially penalized nonqualified withdrawals.