{kind=link}

Think settling your debts for pennies on the dollar is the fastest path to savings?

It can feel that way, but the real math and risks tell a different story.

If you can qualify for a consolidation loan and make steady payments, consolidation usually saves more overall and keeps your credit intact.

Debt settlement cuts your balance but brings hefty fees, possible tax bills, and years of credit damage.

Short version: consolidate if you can afford reliable payments; consider settlement only as a last resort when accounts are already delinquent.

Key Differences Between Debt Consolidation and Debt Settlement Explained

Debt consolidation means taking out a new loan or credit product to pay off multiple existing debts. You’re replacing several monthly bills with one payment and, if things go right, lowering your interest rate. The catch? You still repay the full amount you borrowed, just under better terms. Debt settlement is a different animal. You’re negotiating with creditors to pay less than what you actually owe, usually after you’ve already missed payments. Settlement cuts your principal but typically requires building a lump sum fund over time, and you’ll take serious credit damage in the process.

The core trade off is pretty simple. Consolidation preserves your credit or even improves it if you make on time payments. Settlement can hammer your score and leave derogatory marks visible to lenders for up to seven years. Consolidation works best when you have decent credit and steady income. Settlement is typically considered only when accounts are seriously delinquent and you cannot realistically repay what you owe.

| Method | How It Works | Cost/Fees | Credit Impact | Timeline | Eligibility | Best For |

|---|---|---|---|---|---|---|

| Consolidation | New loan pays off existing debts; single monthly payment | Interest (6.7%–35.99% APR), origination fee (~1%) | Short term dip; long term improvement with on time payments | 12–120 months repayment | Good credit, steady income | Borrowers who can afford payments and want interest savings |

| Settlement | Negotiate reduced balance; pay lump sum or series of payments | Settlement fees 15–25% of total debt; possible tax on forgiven amount | Severe damage; “settled” notation stays up to 7 years | Typically 3–4 years | Poor credit, accounts delinquent or in collections | Borrowers unable to repay in full, facing lawsuits or bankruptcy |

Before choosing a path, weigh these five factors:

Current credit score. Consolidation typically requires fair to good credit (around 720 or higher for favorable rates). Settlement is often pursued when credit is already damaged.

Ability to make monthly payments. If you can afford regular payments, consolidation is usually safer and cheaper in the long run.

Delinquency status. Settlement makes sense primarily when accounts are already past due or in collections.

Interest savings potential. Calculate whether a consolidation loan APR is meaningfully lower than your current blended rate.

Risk tolerance and timeline. Settlement trades immediate relief for years of credit harm and unpredictable negotiation outcomes. Consolidation offers a clear payoff schedule.

Understanding How Debt Consolidation Works

Debt consolidation streamlines your unsecured debts by bundling them into a single new loan or line of credit. The goal is to secure a lower interest rate than what you’re currently paying, reduce the number of monthly bills you juggle, and create a predictable payoff timeline. You apply for new credit, get approved, use those funds to pay off your existing balances in full, then make one monthly payment on the new loan until it’s cleared.

Most borrowers choose a personal loan for consolidation. Personal loan APRs currently range from about 6.7% to 35.99%, with loan amounts available from $1,000 up to $250,000 and repayment terms spanning 12 to 120 months. If you have good or excellent credit, you’re more likely to qualify for a rate below the average credit card APR of roughly 24.80%. That can translate into hundreds or thousands saved on interest. Funding is typically fast. Same day to three days after approval.

Consolidation only makes sense financially if your new loan’s interest rate and any origination fees result in lower total costs than your current debts combined. Many lenders charge an origination fee around 1% of the loan amount, so include that in your calculations. If your credit isn’t strong enough to get a competitive rate, consolidation can actually cost you more and extend your payoff unnecessarily.

Common consolidation methods include:

Personal loan. Unsecured installment loan with fixed interest and term. Widely available through banks, credit unions, and online lenders.

Balance transfer credit card. Move high interest card balances to a new card offering 0% APR for a promotional period (up to 21 months), then pay off before the promo expires.

Home equity loan. Borrow against your home’s equity at a fixed rate. Puts your home at risk if you miss payments.

Home equity line of credit (HELOC). Revolving line of credit secured by your home. Variable rates sometimes start as low as 6.49% APR.

401(k) loan. Borrow from your retirement account. No credit check, but you lose investment growth and face taxes and penalties if you leave your job before repaying.

Cash out refinance. Replace your mortgage with a larger loan and use the difference to pay off debts. Ties unsecured debt to your home.

Understanding How Debt Settlement Works

Debt settlement involves negotiating with creditors to accept less than the full balance you owe, typically in exchange for a lump sum payment or a series of agreed upon payments. The process usually starts after you’ve already missed payments or are in collections, because creditors are more willing to settle when they believe full repayment is unlikely. Settlement companies often advise you to stop making payments entirely so interest and fees pile up while you save cash in a separate account to fund future settlement offers.

Once you’ve accumulated enough savings, a settlement negotiator contacts each creditor with an offer to pay a reduced amount, commonly 40% to 60% of the outstanding balance, in return for marking the account as settled. Creditors are not required to accept, and the process can take months or even years. If a creditor agrees, you pay the negotiated sum and the remaining balance is forgiven. That forgiven amount, if over $600, is often treated as taxable income by the IRS. You could owe taxes on money you never actually received.

You can pursue settlement on your own by calling creditors directly, explaining your financial hardship, and proposing a realistic payment. DIY settlement avoids third party fees but requires persistence, negotiation skills, and the willingness to handle collection calls. Professional settlement companies charge fees typically ranging from 15% to 25% of the total debt you enrolled, plus possible administrative or monthly maintenance fees.

Settlement carries significant risks:

Lawsuits and judgments. Creditors may sue you for unpaid balances before or during settlement negotiations, potentially leading to wage garnishment.

Severe credit damage. Accounts settled for less than the full amount appear as derogatory marks on your credit report for up to seven years.

Tax liability. Forgiven debt over $600 is generally reported to the IRS on Form 1099-C and counted as taxable income.

Collection calls and stress. While negotiating, creditors and collection agencies will continue calling and may escalate efforts.

Unpredictable outcomes. No guarantee creditors will settle, and the total time and final cost remain uncertain.

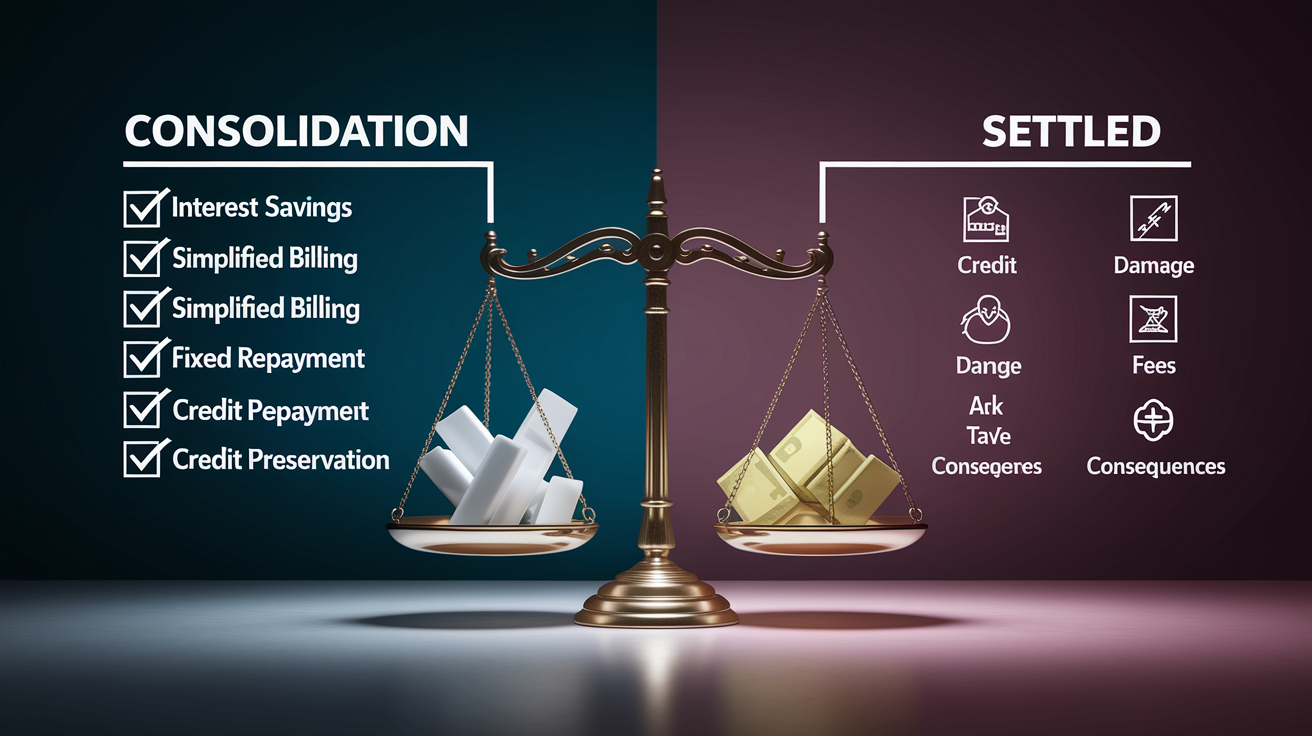

Pros and Cons of Debt Consolidation Compared to Settlement

Debt Consolidation Pros:

Interest savings. Lower APR can reduce total interest paid by hundreds or thousands of dollars over the loan term.

Simplified billing. One monthly payment replaces multiple due dates, reducing missed payment risk.

Fixed repayment schedule. Predictable payoff timeline and monthly amount.

Credit preservation. On time payments can improve your credit score over months to years.

No principal reduction required. You repay the full amount borrowed, maintaining creditor relationships.

Fast funding. Personal loans can fund within one to three days, letting you pay off high interest debts immediately.

Debt Consolidation Cons:

Credit requirements. Good to excellent credit usually needed to qualify for rates below current card APRs.

Upfront costs. Origination fees (around 1%) and closing costs for home secured loans reduce net savings.

Doesn’t address spending habits. Consolidation alone won’t prevent future overspending or new debt accumulation.

Risk with secured loans. Home equity loans and HELOCs put your home at risk if you miss payments.

Longer payoff possible. Extending the term lowers monthly payments but can increase total interest paid.

Hard credit inquiry. Applying for new credit temporarily lowers your score by a few points.

Debt Settlement Pros:

Principal reduction. Potential to eliminate thousands of dollars from original balances.

Avoid bankruptcy. May prevent the need to file Chapter 7 or Chapter 13.

Short term cash flow relief. Stopping payments while saving for settlement frees up monthly cash.

Last resort option. Can resolve debts you genuinely cannot afford to repay in full.

Negotiated finality. Once settled, the account is closed and the creditor cannot pursue the forgiven balance.

Debt Settlement Cons:

Severe credit damage. “Settled for less” notations remain on your credit report for up to seven years and significantly lower your score.

High fees. Settlement companies charge 15% to 25% of enrolled debt, plus possible monthly or administrative fees.

Tax consequences. Forgiven amounts over $600 are often taxable as income, creating an unexpected tax bill.

No guarantee. Creditors may refuse to settle or may sue before negotiations conclude.

Continued collection activity. Stopping payments invites calls, letters, and potential lawsuits.

Longer timeline. Professional settlement programs typically take three to four years to complete.

Comparing Credit Score Impact in Debt Consolidation vs Debt Settlement

Debt consolidation causes a small, temporary credit score dip when the lender runs a hard inquiry and when the new account first appears on your report. However, paying off revolving credit card balances immediately lowers your credit utilization ratio (the percentage of available credit you’re using), which is a major FICO scoring factor. If you make all loan payments on time, your payment history strengthens month by month, and your score typically recovers and improves within six to 24 months.

Debt settlement inflicts serious and lasting harm. The process usually begins with missed or stopped payments, which generate 30, 60, 90, and 120 day delinquency marks. Each late payment can drop your score significantly. When a creditor agrees to settle, the account is reported as “settled for less than the full balance” or similar language, a derogatory notation that signals to future lenders you did not honor your original agreement. That mark stays on your credit report for up to seven years from the date of first delinquency.

Even after settlement, lenders view settled accounts negatively. Someone with a recent settlement on their report will face higher interest rates, lower credit limits, and possible denials for new credit, mortgages, or even rental applications. Settlement makes sense only when your credit is already damaged and you prioritize debt relief over creditworthiness in the near term.

| Method | Short Term Impact | Long Term Impact | Reporting Duration | FICO Factors Affected | Typical Candidate Profile |

|---|---|---|---|---|---|

| Consolidation | Small score drop from hard inquiry and new account; utilization improves | Score improvement if payments are on time; positive payment history builds | Account remains as long as open; paid off accounts reported for 10 years | Payment history, utilization, new credit, credit mix | Good credit, steady income, wants to preserve or improve score |

| Settlement | Severe drop from missed payments, defaults, and settled notations | Derogatory marks linger; score recovery slow and difficult | Settled accounts and late payments stay up to 7 years | Payment history, amounts owed, derogatory marks | Poor credit, accounts delinquent, cannot afford full repayment |

Cost Breakdown: Fees, Interest, and Tax Considerations for Each Option

When you consolidate debt with a personal loan, your primary cost is interest. If you shift $10,000 of credit card debt carrying an average APR of 25% to a personal loan at 19% APR over five years, you’ll pay roughly $5,564 in interest instead of about $7,610. A savings of around $2,046 or 27%. That’s the upside. The downside is origination fees, which typically run about 1% of the loan amount. On a $10,000 loan, that’s $100 deducted upfront, reducing your net savings. Balance transfer cards often charge a transfer fee of 3% to 5%, so moving $10,000 could cost $300 to $500 before you even start paying down principal.

Home equity loans and HELOCs come with closing costs similar to a mortgage. Appraisal fees, title searches, and legal fees that can total hundreds or even low thousands of dollars. While the interest rates can be attractive (some HELOCs advertise rates as low as 6.49% APR), the risk is real. Your home becomes collateral, and missed payments can lead to foreclosure.

Debt settlement costs are structured differently. Professional settlement companies charge fees equal to 15% to 25% of the total debt you enroll. If you enroll $20,000 in debt and settle it for $10,000, you’ll pay the creditor $10,000 and the settlement company roughly $3,000 to $5,000 in fees. That brings your total outlay to $13,000 to $15,000, still less than the original $20,000 but not the “pennies on the dollar” often advertised. More importantly, the IRS treats forgiven debt over $600 as taxable income. In this example, the $10,000 forgiven is reported on Form 1099-C, and you’ll owe federal and possibly state income tax on that amount. Potentially another $2,000 to $3,000 depending on your tax bracket.

Before choosing, compare these cost factors:

APR differential. Calculate the difference between your current blended interest rate and the consolidation loan APR.

Origination and transfer fees. Add these to your total cost. They reduce net savings.

Settlement company fees. Typically 15–25% of enrolled debt, plus any monthly or setup charges.

Tax liability on forgiven debt. Budget for income tax on any amount forgiven above $600.

Opportunity cost. Stopping payments during settlement allows interest and late fees to compound, increasing the total balance creditors will later negotiate.

Eligibility Criteria for Debt Consolidation and Debt Settlement

Debt consolidation lenders want to see good credit, stable income, and a manageable debt to income ratio. Most favorable personal loan rates go to borrowers with credit scores of 720 or higher. If your score is below that threshold, you’ll likely face APRs in the mid to high teens or even above 30%, which can eliminate the benefit of consolidation. Lenders also verify employment and income to confirm you can afford the new monthly payment. A high debt to income ratio, typically above 43%, may disqualify you or push you toward higher rates.

Debt settlement, by contrast, has no formal credit score requirement because you’re not borrowing new money. Settlement companies and creditors are more interested in whether you’re already behind on payments and whether you can realistically save enough to fund a lump sum offer. Many settlement firms require a minimum total debt amount, often $7,500 to $10,000, to justify the administrative effort and fees. If you’re current on all accounts and have decent credit, settlement is usually not appropriate and will only harm your financial standing unnecessarily.

Red flag disqualifiers to watch for:

Consolidation. Credit score below lender minimums, unstable or insufficient income, debt to income ratio above lender limits, recent bankruptcy or foreclosure, too many recent hard inquiries.

Settlement. Total debt below company minimums, accounts fully current with no hardship, inability to set aside monthly savings for settlement fund, unwillingness to accept credit damage and tax consequences, creditor actively garnishing wages (settlement may not stop legal action already in motion).

Timelines for Debt Consolidation vs Debt Settlement

A debt consolidation loan moves quickly once approved. Many online lenders and credit unions fund personal loans same day or within one to three business days. Balance transfer credit cards can provide a credit line immediately upon approval, though the transfer itself may take a few days to post. Once your old balances are paid off, you’re locked into a fixed repayment term, commonly 12 to 120 months for personal loans, though most borrowers choose terms between two and seven years. The entire process from application to final payoff is predictable and structured.

Balance transfer cards offer a different timeline. Promotional 0% APR periods can last up to 21 months, giving you nearly two years to pay down principal interest free if you qualify. The catch is you must pay off the full transferred balance before the promo expires, or the remaining balance reverts to a standard APR that may be higher than your original cards.

Debt settlement is far less predictable. Professional settlement programs typically advise a timeline of three to four years. During that period, you stop paying creditors and instead deposit money into a dedicated account controlled by the settlement company. Once the account builds enough funds, the company begins negotiating with creditors one by one. Some creditors settle quickly. Others refuse or drag out negotiations. If a creditor sues before settlement is reached, the timeline and strategy can shift dramatically.

DIY settlement can be faster if you already have a lump sum saved and creditors are willing to negotiate immediately, but there’s no guarantee. You might resolve one account in weeks and spend months on another. Throughout the process, interest and late fees continue to accrue on unpaid balances, and collection activity intensifies.

Real Examples Demonstrating When Consolidation or Settlement Is Better

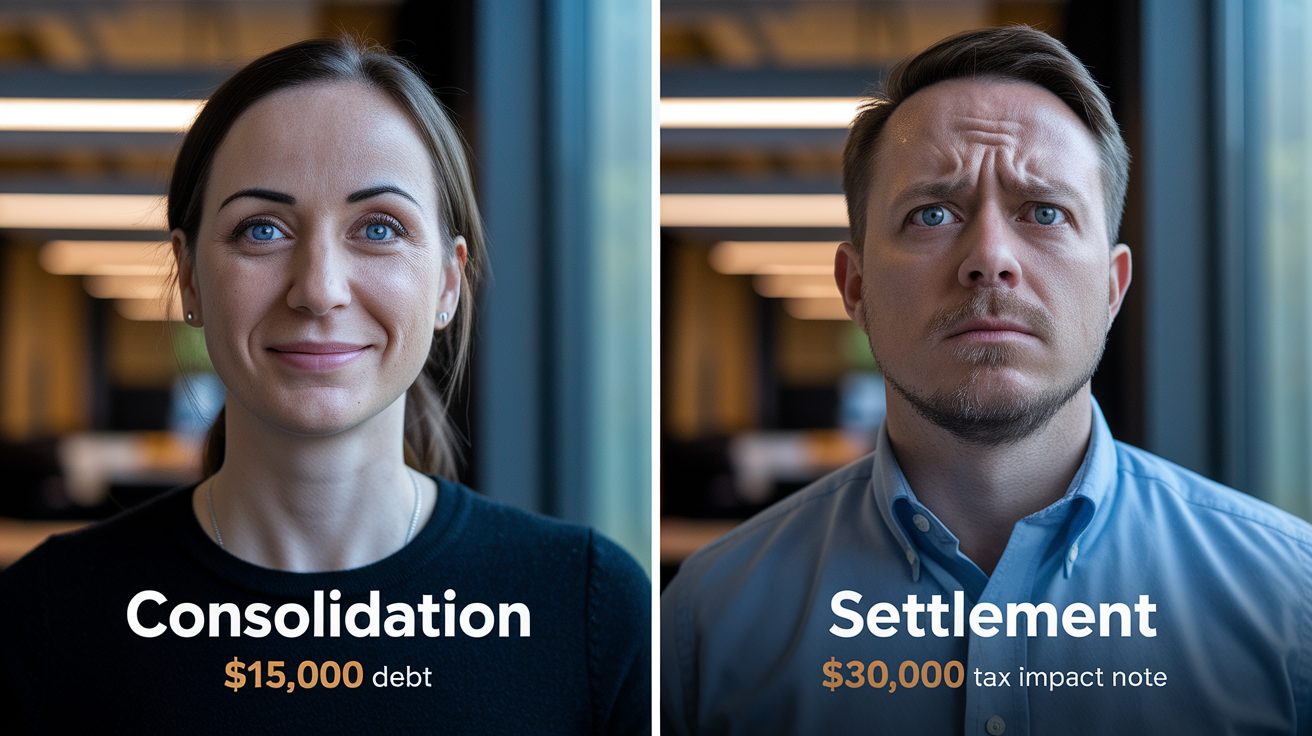

Scenario 1: Consolidation

Sarah has $15,000 spread across three credit cards with APRs of 22%, 26%, and 28%. Her credit score is 740, and she earns a steady $55,000 annually. She applies for a personal loan and is approved for $15,000 at 13% APR over five years. Her new monthly payment is $342. Under her old minimum payments, she was paying roughly $450 per month and would have taken over 15 years to pay off the debt while paying more than $12,000 in interest. With the consolidation loan, she’ll pay about $5,500 in interest and be debt free in five years. Her credit utilization drops immediately, her score improves within six months, and she avoids late payments and collection calls.

Scenario 2: Settlement

Mark owes $30,000 across four credit cards, all more than 90 days past due. His credit score has fallen to 520, and he lost his job six months ago. He cannot qualify for a consolidation loan and is facing potential lawsuits. He enrolls in a debt settlement program and agrees to deposit $400 per month into a settlement account. After two years, he’s saved $9,600. The settlement company negotiates with his creditors and settles the $30,000 for a total of $15,000. Mark pays $15,000 to creditors and about $5,250 in settlement fees (17.5% of original debt). The $15,000 forgiven is reported to the IRS as income, creating a tax bill of roughly $3,300 at his marginal rate. His total cost is approximately $23,550, saving him about $6,450 compared to the original $30,000. However, his credit report now shows four settled accounts, each marked “settled for less,” and those notations will remain for seven years from the date of first delinquency.

Which profile fits your situation:

Choose consolidation if you have fair to good credit, steady income, and can afford monthly payments that will retire the debt in a reasonable time.

Consider settlement only if accounts are already delinquent, your credit is poor, you cannot realistically repay in full, and you’re willing to accept years of credit damage and possible tax consequences.

Avoid settlement if you’re current on payments or have the income and credit to qualify for consolidation. Settlement will harm your financial profile unnecessarily.

Explore alternatives first. Nonprofit credit counseling, debt management plans, or even bankruptcy if debts are truly unmanageable and settlement fees and taxes won’t provide meaningful relief.

Alternatives to Debt Consolidation and Debt Settlement

The debt snowball method focuses your energy on the smallest balance first. You make minimum payments on all accounts except the one with the lowest balance, which you attack with every extra dollar. Once that’s paid off, you roll the freed up payment into the next smallest debt. The psychological wins from clearing accounts quickly can keep you motivated, even though you’ll pay slightly more interest than the avalanche method.

The debt avalanche targets the highest interest debt first while paying minimums on everything else. Mathematically, this saves the most money over time because you eliminate the costliest debt fastest. It requires patience. The first payoff may take longer, but the total interest paid is minimized.

A debt management plan (DMP) offered through a nonprofit credit counseling agency consolidates your unsecured debts into a single monthly payment without requiring a new loan. The counselor negotiates with creditors to lower interest rates and waive certain fees, then you make one payment to the agency, which distributes funds to creditors. DMPs typically last three to five years, cost a setup fee and monthly maintenance fee (often capped around $75 total), and require you to close the enrolled credit card accounts. Your credit report will show you’re in a DMP, but there’s no “settled” notation, and the impact is less severe than settlement.

Bankruptcy is the last resort. Chapter 7 bankruptcy liquidates non exempt assets to pay creditors and discharges most unsecured debts. It’s available to lower income filers or those who pass a means test. Chapter 13 reorganizes debts into a court supervised repayment plan lasting three to five years, allowing you to keep assets like your home while catching up on secured debts. Both options devastate your credit score and remain on your report for seven (Chapter 13) to ten (Chapter 7) years, but they provide a legal fresh start when no other option is viable.

| Alternative | How It Works | Timeline | Credit Impact | Best For |

|---|---|---|---|---|

| Debt Snowball | Pay smallest balance first; roll payments into next smallest | Varies by balances and budget | Neutral to positive if payments remain on time | Borrowers needing motivational wins and quick progress |

| Debt Avalanche | Pay highest interest debt first; minimize total interest | Varies by balances and budget | Neutral to positive if payments remain on time | Borrowers focused on math and maximum savings |

| Debt Management Plan (DMP) | Credit counselor negotiates lower rates; single payment to agency | 3–5 years | Moderate; DMP notation appears; less severe than settlement | Borrowers who need lower rates and structure but want to repay in full |

| Bankruptcy (Ch. 7 / Ch. 13) | Legal discharge or court supervised repayment; fresh start | Ch. 7: months; Ch. 13: 3–5 years | Severe; remains on report 7–10 years | Borrowers with unmanageable debt and no viable repayment option |

Expert Recommendations on Choosing Between Consolidation and Settlement

Financial advisors consistently recommend consolidation over settlement whenever the borrower can qualify and afford the payments. Consolidation preserves credit, avoids tax complications, and provides a clear path to becoming debt free. Settlement should be considered only when consolidation is genuinely not an option. When credit scores are too low, income is insufficient, or accounts are already in collections and creditors are threatening legal action.

Before committing to either path, pull your credit report from all three bureaus and check your FICO score. If your score is above 680, focus your energy on consolidation options and compare offers from multiple lenders to find the lowest APR and best terms. If your score is below 600 and accounts are delinquent, settlement or a debt management plan may be your realistic choices, but consult a nonprofit credit counselor first to explore all angles.

Calculate the total cost of each option including fees, interest, and taxes. For consolidation, add up the interest you’ll pay over the loan term plus any origination or transfer fees, then compare that to what you’d pay under your current payment schedule. For settlement, estimate the settlement amount (often 40–60% of balances), add company fees (15–25% of enrolled debt), and budget for income tax on forgiven amounts over $600. If the numbers are close, the credit score impact should tip the scale toward consolidation.

Here’s a five step decision framework:

- Check your credit score and report. Scores above 720 open consolidation options with favorable rates. Scores below 600 often mean settlement is the only non bankruptcy path.

- Assess your monthly income and budget. If you can afford a structured monthly payment that will retire the debt in five to seven years, consolidation is safer and cheaper long term.

- Evaluate debt severity and delinquency. Accounts current or only slightly behind favor consolidation. Accounts 90+ days past due or in collections push toward settlement.

- Compare total costs and timelines. Run the math on interest, fees, and taxes. Factor in how long you’re willing to carry the debt and the credit report impact duration.

- Measure your risk tolerance. Settlement is unpredictable, exposes you to lawsuits and tax bills, and damages credit for years. Consolidation offers certainty and credit preservation if you can qualify.

Final Words

In the action, you saw the main differences: consolidation uses new credit or a balance-transfer to lower interest and simplify payments, while settlement requires missed payments, builds a cash reserve, and often cuts principal at the cost of fees, tax consequences, and long credit damage.

If you can qualify for a consolidation loan or 0% transfer, start there. If you’re deeply delinquent and out of options, settlement can be a last resort. Use the decision factors we covered to choose between debt consolidation vs debt settlement, and take the small, steady steps that rebuild credit and calm your budget.

FAQ

Q: What two debts cannot be erased?

A: The two debts that typically cannot be erased in bankruptcy are child support and most student loans, with very limited exceptions and rare hardship discharges.

Q: How much is the payment on a $50,000 consolidation loan?

A: The payment on a $50,000 consolidation loan depends on rate and term. For 60 months, about $980 at 6.7% APR and about $1,460 at 24.8% APR; longer terms lower monthly cost but raise total interest.

Q: How to pay $30,000 debt in one year?

A: To pay $30,000 in one year, aim for about $2,500 monthly and build a tight budget, increase income, cut nonessential spending, sell items, use lower-rate consolidation if it saves interest, and apply windfalls.

Q: Why does Dave Ramsey not recommend debt consolidation?

A: Dave Ramsey does not recommend debt consolidation because it can mask spending habits, extend repayment, and add fees; he favors the debt snowball to build momentum and force behavior change.