{kind=link}

Which saves you more money: a debt consolidation loan or credit counseling?

Both cut what you pay, but the winner comes down to your credit score and the interest rates you can get.

If you can lock a consolidation loan rate well below your current card average, say 8% instead of 18%, a loan usually saves the most (which can save thousands on $25,000).

If your score is low or cards charge 15% to 25%, credit counseling and a debt management plan often cut interest and fees more.

Rule: score 670+? Shop lenders. Otherwise, call a nonprofit counselor.

Choosing Between Debt Consolidation Loans and Credit Counseling

A debt consolidation loan is a new personal loan you take out to pay off multiple debts. You’re left with one fixed monthly payment to a single lender. Credit counseling connects you with a nonprofit that helps you build a budget, negotiate lower interest rates with your existing creditors, and set up a debt management plan. No new loan required.

Your credit profile and the kind of support you need will determine which one makes sense. Debt consolidation loans tend to work best if you’ve got good credit (scores around 670 or higher), stable income, and can qualify for an interest rate lower than what you’re currently paying. Often that’s around 10% or less to see real savings. Credit counseling and debt management plans work well when your credit’s damaged, your card rates are high (15% to 25%+), or you need hands-on help creating a realistic budget and actually sticking to a payoff plan.

If you can lock in a low rate and trust yourself not to run up new balances, a consolidation loan simplifies payments and might cut your interest costs. If you’re struggling to make minimums, facing collections, or unsure how to prioritize debts, credit counseling gives you professional negotiation and structure without requiring a high credit score.

| Option | Best For | Key Advantage | Typical Drawback |

|---|---|---|---|

| Debt Consolidation Loan | Good credit, stable income, multiple high-interest debts | Potentially lower interest rate; single fixed payment | Requires qualifying; risk of adding new debt on open cards |

| Credit Counseling / DMP | Damaged credit, high rates, need budgeting support | Negotiated rate reductions; no new loan; professional guidance | Cards typically closed; monthly fees; 3–5 year commitment |

How Debt Consolidation Loans Work

A debt consolidation loan is a personal loan you use to pay off credit cards, medical bills, or other unsecured debts. Once you’re approved, the lender sends you the loan proceeds (either directly to your creditors or into your bank account) and you repay the lender over a fixed term. Usually two to seven years.

Lenders check your credit score, income, and debt-to-income ratio to decide whether to approve you and what interest rate to offer. Better credit typically unlocks lower rates. If your score’s below 620 or your income’s unstable, you might not qualify. Or you may be offered a rate higher than your current debts, which defeats the purpose.

The process follows a predictable sequence.

Shop and compare offers. Check rates from banks, credit unions, and online lenders. Many allow prequalification without a hard credit pull so you can see estimated terms before applying.

Submit a formal application. Provide proof of income (pay stubs, tax returns), photo ID, and authorize a hard credit inquiry that may temporarily lower your score by a few points.

Review loan terms and sign. Confirm the APR, monthly payment, total interest, origination fee (often around 1% of the loan), and repayment term before accepting.

Receive funds and pay creditors. Some lenders send payments directly to your creditors. Others deposit the money into your account and you make the payments yourself.

Make fixed monthly payments. Your new loan has a set payment schedule. Stick to it to avoid late fees and protect your credit.

If you secure a rate meaningfully lower than your current average (say, 8% on a consolidation loan versus 18% across multiple cards), you’ll save on interest and may pay off the debt faster. Especially if you avoid charging new balances.

How Credit Counseling and Debt Management Plans Work

Credit counseling organizations are typically nonprofit agencies that offer free or low-cost budget reviews, financial education, and debt advice. A certified counselor evaluates your income, expenses, and debts, then helps you create a realistic spending plan and explore options. That might include a debt management plan, a consolidation loan referral, debt settlement, or even bankruptcy if that’s the most responsible path.

A debt management plan (DMP) is a structured repayment program the counselor sets up with your creditors. You make one monthly payment to the counseling agency, and they distribute the money to your creditors according to negotiated terms. Creditors often agree to lower or eliminate interest charges and waive certain fees as part of the plan, which can dramatically reduce the time and cost to pay off your balances.

Core features of a DMP:

Negotiated interest-rate reductions. Creditors may drop rates to as low as 0%–8%, compared to typical card rates of 15%–25%.

Single monthly payment. You send one payment to the agency. They handle distributing funds to each creditor on schedule.

Fixed timeline. Most DMPs run three to five years, with a clear payoff date from the start.

Account restrictions. You typically can’t use credit cards enrolled in the plan, and creditors may close those accounts to prevent new charges.

Counseling agencies charge modest fees, often a one-time setup fee of $30 to $50 and a monthly administration fee of $20 to $75. Capped by state law at no more than $79 per month in many jurisdictions. The initial counseling session’s usually free, with no obligation to enroll.

Cost Comparison: Fees, Interest Rates, and Long‑Term Expense

Understanding what you’ll pay over the life of each option helps you choose the one that saves the most money. Debt consolidation loans involve interest charges and sometimes an origination fee deducted from the loan proceeds. Credit counseling and debt management plans include setup and monthly administrative fees, but creditors often agree to reduce or waive interest, which can offset those costs.

| Option | Upfront Cost | Ongoing Cost | Interest Impact |

|---|---|---|---|

| Debt Consolidation Loan | Origination fee ~1% of loan; hard credit inquiry | Fixed monthly payment includes principal + interest | Rate depends on credit score; must be lower than current debts to save |

| Credit Counseling / DMP | Setup fee $30–$50 (state-regulated; sometimes waived) | Monthly admin fee $20–$75 (capped at $79 federally) | Creditors often reduce rates to 0%–8%; total interest savings can be substantial |

If you qualify for a consolidation loan at 8% and your current card balances carry 20% APRs, the loan will cut your interest expense significantly, even after paying a 1% origination fee. But if your credit only qualifies you for a 15% loan rate, you may not save much compared to your existing debts.

With a DMP, you’ll pay counseling fees totaling roughly $240 to $900 per year. But negotiated interest reductions can save thousands. For example, dropping from an average 18% rate to 5% on $25,000 in debt over four years saves far more in interest than you spend on monthly fees.

Impact on Credit Scores

Taking out a debt consolidation loan triggers a hard inquiry on your credit report, which can lower your score by a few points temporarily. Opening a new installment account also reduces the average age of your credit, which may ding your score slightly in the short term. But if you use the loan to pay off revolving credit-card balances, your credit utilization ratio drops. That often results in a score increase within a few months, assuming you make on-time payments and don’t rack up new card debt.

Credit counseling itself doesn’t appear on your credit report and won’t hurt your score. Enrolling in a debt management plan also doesn’t directly damage credit, but the actions tied to the plan can have indirect effects. Creditors participating in a DMP typically close the enrolled accounts to prevent new charges, which can raise your overall credit utilization if those were your only cards. Losing available credit and shortening your credit history may cause a temporary score dip.

Over the longer term, both options can help rebuild credit if managed responsibly. Consistent on-time payments to a consolidation loan improve your payment history, the most influential credit-score factor. A DMP establishes a track record of reliable payments distributed by the counseling agency, and once you complete the plan and your balances hit zero, your utilization falls and your score often recovers. Sometimes surpassing where it started, especially if missed or late payments were dragging it down before you enrolled.

The key difference: a consolidation loan offers faster credit-score upside if you qualify for favorable terms and keep cards paid off, while a DMP prioritizes getting out of debt even if your score takes a small hit initially.

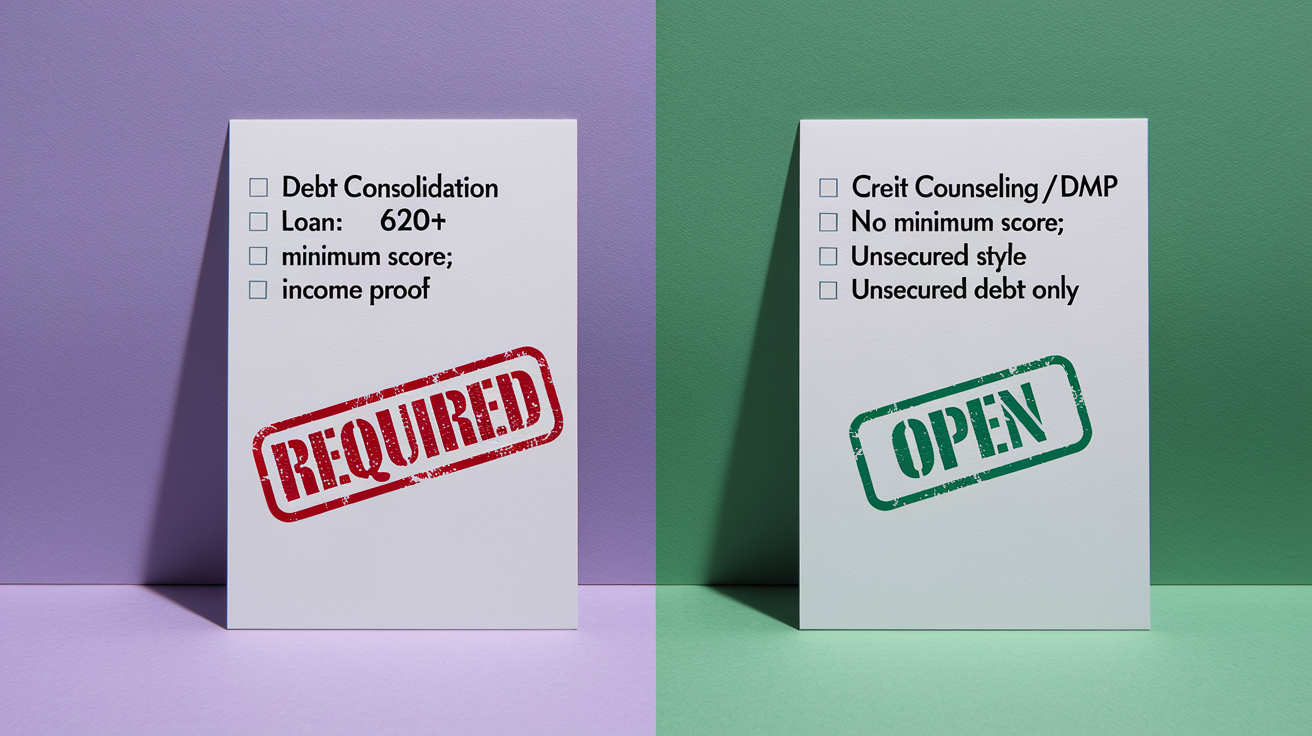

Eligibility Requirements for Each Option

Qualifying for a debt consolidation loan depends on your creditworthiness and income stability. Lenders want confidence you’ll repay the new loan, so they examine your credit report, score, employment history, and how much debt you already carry relative to your income.

Common lender requirements include a minimum credit score (often 620 or higher, though some lenders set the bar at 660–680 for better rates), proof of steady income through pay stubs or tax returns, and a debt-to-income ratio below 40%–50%. Lenders also verify your identity with a government-issued ID and may ask for bank statements to confirm you can afford the monthly payment.

Credit counseling has no minimum credit score, income threshold, or employment requirement to participate in an initial consultation. Nonprofit agencies are designed to help anyone struggling with debt, regardless of credit history. But enrolling in a debt management plan requires creditor approval. Your creditors must agree to accept reduced payments and lower interest rates, and not all creditors participate in DMPs.

Basic requirements for credit counseling and DMP enrollment:

Willingness to share financial details. Income, expenses, debts, and spending habits so the counselor can build an accurate budget.

Unsecured debt only. Most DMPs handle credit cards, personal loans, and medical bills. Secured debts like mortgages and car loans are excluded.

Ability to afford the negotiated payment. The counselor calculates a monthly amount you can realistically pay. If your income’s too low or expenses too high, a DMP may not be feasible and the counselor will recommend alternatives.

Consolidation loans require good credit and income to qualify for savings. Credit counseling’s accessible to almost anyone, though DMP success depends on creditor cooperation and your ability to commit to the payment plan.

Expected Timelines to Become Debt‑Free

Debt consolidation loans typically offer repayment terms ranging from two to seven years (24 to 84 months), with the exact timeline depending on the loan amount, interest rate, and lender. Shorter terms mean higher monthly payments but less total interest paid. Longer terms reduce the monthly burden but increase the overall cost. Many borrowers choose three- to five-year loans as a middle ground between affordability and efficient payoff.

Debt management plans generally run three to five years (36 to 60 months), structured to pay off your enrolled debts in full at the negotiated lower interest rates. The counselor and creditors agree on a timeline that balances what you can afford each month with getting you out of debt as quickly as possible. In practice, most people complete a DMP in around four years.

If you’re comparing the two, the timelines are often similar. Both tend to land in the three-to-five-year range. The difference lies in flexibility: with a consolidation loan you can sometimes choose a shorter or longer term upfront, while a DMP timeline’s set by the counselor and creditors based on your total debt and monthly payment capacity. Either way, expect to commit several years to the payoff process. Finishing early (by making extra payments on a loan or increasing DMP contributions if allowed) can shorten the timeline and reduce total interest.

When a Debt Consolidation Loan Is the Better Choice

A debt consolidation loan makes the most sense when your credit and income position you to save money through a lower interest rate and you can handle a fixed monthly payment without ongoing support. If the numbers work in your favor and you’re confident in your budgeting discipline, a loan simplifies your finances and may cost less over time than continuing to pay high card rates or enrolling in a fee-based debt management plan.

Consider a consolidation loan if your credit score is good to excellent (typically 670+), giving you access to loan rates around 6%–12%. Well below typical credit-card APRs of 15%–25%.

You have stable, verifiable income and a debt-to-income ratio lenders find acceptable, making approval likely.

Your current debts carry high interest rates and consolidating into one lower-rate loan will produce clear savings, even after any origination fee.

You’re disciplined enough to avoid new debt once cards are paid off. The risk with consolidation is charging up the cards again and ending up with both the loan and new balances.

When these conditions align, a consolidation loan can cut your interest costs, simplify bill-paying to one due date, and potentially improve your credit score as revolving balances drop and on-time installment payments accumulate.

When Credit Counseling Is the Better Choice

Credit counseling and a debt management plan become the better option when you can’t qualify for a low-rate consolidation loan, your debts are overwhelming, or you need professional help building a sustainable budget and sticking to a payoff strategy. Counseling doesn’t depend on a high credit score, and the negotiated interest reductions can deliver savings even if your credit history would disqualify you from favorable loan terms.

Choose credit counseling and consider enrolling in a DMP if your credit score’s damaged or too low to qualify for a consolidation loan with an interest rate lower than your current debts.

You’re struggling to make minimum payments or have accounts in collections, and creditors are more likely to negotiate through a nonprofit counselor than offer you new credit.

You need budgeting guidance and accountability, not just a new loan. Counselors provide education, spending plans, and ongoing check-ins to address the root causes of debt.

You want creditor-negotiated rate reductions without taking on new debt, and you’re willing to have enrolled credit cards closed and commit to a structured three-to-five-year repayment plan.

Nonprofit credit counseling agencies are also required to recommend the best solution for your situation, even if that means referring you to a consolidation loan, settlement company, or bankruptcy attorney instead of enrolling you in a DMP. That obligation to act in your interest makes counseling a safe first step if you’re unsure which path fits your circumstances.

Expert Guidance and How to Choose the Right Path

Financial advisors and credit counselors use a decision framework that weighs your credit profile, debt load, income stability, and personal discipline to recommend the option most likely to get you out of debt at the lowest total cost. The goal is to match the solution to your real-world ability to execute it, not to push you into the product with the highest profit margin.

Key factors professionals consider when guiding clients:

Credit score and loan qualification. If you can secure a rate of roughly 10% or lower, consolidation often wins on cost. If your score only qualifies you for rates above 15%, a DMP’s negotiated reductions may save more.

Debt-to-income ratio and monthly affordability. Lenders cap approval based on DTI. Counselors structure DMP payments around what you can realistically afford, making DMPs accessible even when loans aren’t.

Behavioral track record. If you’ve previously paid off cards only to max them out again, a DMP’s forced account closures and counselor oversight can prevent that cycle. If you have strong spending discipline, a loan offers more flexibility.

Types of debt. Consolidation loans and DMPs both handle unsecured debts. If you also carry secured debts (mortgage, auto) or tax obligations, those require separate strategies and may tip the recommendation.

Timeline and life circumstances. A shorter loan term can free you faster but demands higher payments. A DMP’s three-to-five-year structure may fit better if your budget’s tight or income variable.

Start by checking your credit score and requesting loan prequalification offers to see what rates you can access without a hard inquiry. Compare those rates to your current debt APRs and calculate total interest over the life of each option, including any fees. If the loan saves you significant money and you’re confident you won’t add new debt, that’s often the cleaner path. If loan rates aren’t favorable, or you recognize you need help with budgeting and creditor negotiation, contact a certified nonprofit credit counseling agency for a free evaluation. They’ll walk through your full financial picture and recommend consolidation, a DMP, settlement, or another option based on what actually works for your situation.

Final Words

You’ve seen the key difference: consolidation loans combine balances into one fixed payment, while credit counseling creates a budget, negotiates rates, and sets a debt management plan.

Quick rule: good credit and steady income lean toward a consolidation loan. Overwhelmed or high-interest debt? Credit counseling often gives structure and negotiation help.

Use debt consolidation loan vs credit counseling as your comparison tool, pick what lowers cost and keeps you paying on time. Do one thing this week: check a loan rate or call a nonprofit counselor, and you’ll be moving forward.

FAQ

Q: Is credit counseling the same as debt consolidation?

A: Credit counseling is not the same as debt consolidation. Counseling builds a budget and may set up a debt management plan (no new loan); consolidation combines multiple debts into one new loan with different costs and risks.

Q: How much is the payment on a $50,000 consolidation loan?

A: The payment on a $50,000 consolidation loan depends on interest and term. Rough examples: 6% for 5 years ≈ $970/month; 8% for 5 years ≈ $1,014/month; 10% for 7 years ≈ $830/month.

Q: Why does Dave Ramsey not recommend debt consolidation?

A: Dave Ramsey doesn’t recommend debt consolidation because he prefers paying debts one-by-one without new loans; consolidation can extend repayment, add fees, or use secured debt, which raises risk.

Q: How to pay off $30,000 in debt in 1 year?

A: To pay off $30,000 in one year you need about $2,500 monthly plus interest. Set a strict budget, boost income, target highest-rate balances, make extra payments, and automate transfers.