{kind=link}

Think an 800 credit score is only for people with perfect salaries or secret credit hacks?

It’s not.

Reaching 800 mostly comes down to two things: flawless payments and very low credit utilization (how much of your credit limit you use).

If you focus there first, automate every payment, fix errors on your reports, and pay down balances before statement closing dates, you can move toward an 800 score faster than you expect.

Core Steps to Reach an 800 Credit Score Fastest

An 800 credit score puts you near the top of the FICO range, which runs from 300 to 850. Getting there takes consistent behavior over time, not some quick hack. Payment history makes up 35% of your score and utilization accounts for another 30%, so those two spots give you the fastest improvement when you dial them in. Hard inquiries stick around for 24 months but hit hardest during the first 12, while a single 30-day late can hang on for seven years and tank your score immediately.

Your fastest route? Aggressive focus on payments and balances, plus fixing errors and staying on top of monitoring. Automate every payment so you can’t slip up. Pay balances down below 10% utilization to show FICO you’re handling credit responsibly. When you dispute inaccurate items, bureaus investigate within 30 to 45 days, and corrections can boost your score within one reporting cycle. Keep old accounts open to preserve your credit age. Limit new applications so inquiries don’t pile up.

You can start moving toward 800 right now with clean data and disciplined execution. The actions below are the foundation everything else builds on.

- Pull your full credit report from all three bureaus and flag errors, outdated items, or accounts you don’t recognize.

- Set up automatic payments for every credit obligation so you never miss a due date.

- Pay down revolving balances until your overall utilization drops well below 30%, ideally under 10%.

- Make an extra payment before your statement closing date to lower the balance your issuer reports.

- Avoid opening new accounts unless you really need them, since each hard inquiry and new tradeline temporarily lowers your average account age.

- Keep your oldest credit cards active with small recurring charges, even if you don’t use them for everyday spending.

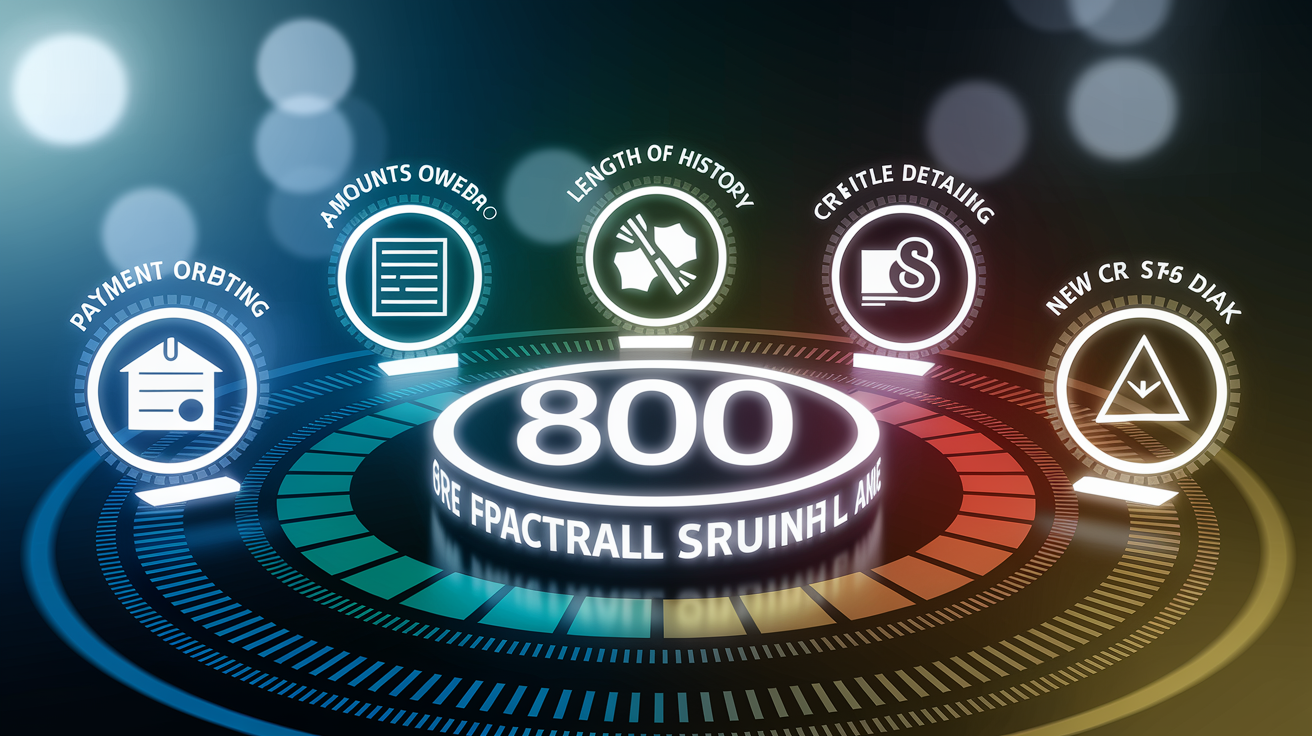

The Five Credit Score Factors at a Glance (Concise Overview)

FICO scoring models weigh five categories of information pulled from your credit report. Payment history carries the most weight at 35%, followed by amounts owed at 30%. The remaining factors (length of credit history, credit mix, and new credit) account for 15%, 10%, and 10% respectively. Together these factors create a composite picture of risk. The balance across all five determines whether you reach 800 or plateau below it.

Late payments and collections remain on your report for seven years. Bankruptcy filings can stay up to ten years for Chapter 7 and seven years for Chapter 13. Hard inquiries from credit applications remain visible for 24 months but typically affect your score only during the first 12 months. Soft inquiries (background checks or your own credit pulls) don’t impact scoring at all.

Optimizing one factor while ignoring another rarely produces an 800 score. The strongest profiles show flawless payment records, minimal utilization, mature account age, diverse credit types, and restrained application activity. Small weaknesses in one area can be offset by strength in others, but consistent excellence across the board is what pushes you into the top tier.

| Factor | Weight % |

|---|---|

| Payment history | 35% |

| Amounts owed (credit utilization) | 30% |

| Length of credit history | 15% |

| Credit mix | 10% |

| New credit (inquiries and recent accounts) | 10% |

Advanced Payment History Recovery & Optimization Tactics

Recovering from past delinquencies demands a clear triage plan. If you’ve got one or two recent late payments, focus first on bringing every account current and maintaining perfect payment behavior going forward. The damage from a late payment diminishes gradually as the mark ages, but only if you build a long stretch of clean months behind it. If multiple accounts fell behind, prioritize the ones with the smallest gaps to avoid additional lates, then systematically catch up the rest.

Goodwill letters and pay-for-delete negotiations offer limited but real pathways to remove negative marks. A goodwill request asks the creditor to remove an isolated late payment as a courtesy, citing your otherwise strong history and any extenuating circumstances. Pay-for-delete involves negotiating with a collection agency to remove the tradeline entirely in exchange for payment. Not all agencies agree to this arrangement and it’s never guaranteed. Always document agreements in writing before sending payment. Keep copies of settlement letters and proof of payment for future disputes if the item doesn’t come off as promised.

Once you’ve addressed past damage, shift focus to high-quality payment patterns. Set reminders a few days before each due date as a backup to automatic payments. Verify that autopay schedules align with your cash flow. Review statements monthly to catch billing errors before they result in missed payments. If you experience temporary financial hardship, contact creditors immediately to explore hardship plans or temporary forbearance rather than letting accounts slide into delinquency.

Advanced recovery and optimization actions include:

Delinquency triage by recency and severity: Bring the newest lates current first to stop the bleeding, then work backward on older accounts.

Rapid rescore through creditor intervention: Some lenders offer expedited reporting of paid-off balances or corrections when you need a score boost before a mortgage or auto loan closes.

Negotiation leverage with collection agencies: Offer lump-sum payment in exchange for deletion or request verification of debt if the account details are incomplete or inaccurate.

Hardship plan documentation: Formal forbearance agreements may pause reporting or prevent further damage during recovery periods.

Aging-out timing strategy: As negative marks approach the seven-year drop-off date, avoid actions that reset the clock, such as making partial payments on very old charged-off accounts without a clear deletion agreement.

Advanced Credit Utilization Optimization Methods

Utilization below 10% consistently appears in profiles scoring 800 and above. Paying down balances is the most direct route, but timing your payments to align with statement closing dates amplifies the effect. Most issuers report your balance to the bureaus on the day your statement generates, so a payment made the day before that closing date lowers the reported balance even if you carry a balance forward into the next cycle.

Managing utilization across multiple cards requires tracking both per-card and portfolio-wide ratios. A single card maxed out can hurt your score even if your overall utilization is low, because FICO also evaluates individual card utilization. Spreading balances evenly across cards, or concentrating spending on one card while keeping others at zero, both work depending on your total available credit and monthly spending patterns. Requesting credit limit increases without new hard pulls can instantly lower your utilization ratio, but only if you avoid increasing your spending to match the new limit.

Precision Utilization Management

Advanced tactics focus on controlling the exact balance reported each cycle. Some cardholders make multiple payments throughout the month to keep their daily balance low. Others use a dedicated card for spending and immediately pay it off, leaving the high-limit cards at zero balances that get reported. Balance transfers can temporarily reshape utilization if you move debt from a maxed card to one with headroom, but transfer fees and promotional-rate expirations require careful planning.

Precision methods include:

Rapid limit-increase timing: Request increases immediately after paying down balances or receiving a raise, when your debt-to-income ratio looks strongest and issuers are most likely to approve without a hard pull.

Statement-cut manipulation: Learn each card’s statement closing date and schedule large payments one or two days before to minimize reported balances.

Targeted balance transfers for utilization shaping: Move balances from cards nearing their limits to cards with lower utilization, improving both per-card and overall ratios without paying down total debt immediately.

Controlled spend-and-wipe cycles: Charge regular expenses to one card, pay the balance before the statement closes, and let the card report a near-zero balance while still showing active use.

Expanding Credit Age With Strategic, Low-Risk Methods

Length of credit history contributes 15% to your FICO score and improves only through patience and careful account management. Closing your oldest card shortens your credit history immediately. Opening new accounts lowers your average age. Preservation of existing accounts takes priority over aggressive credit expansion. Even cards you no longer use daily should remain open with occasional small purchases to prevent issuer closures due to inactivity.

Becoming an authorized user on a parent’s or partner’s long-standing account can add years of history to your profile if the primary cardholder has flawless payment history and low utilization. Verify that the issuer reports authorized-user activity to the bureaus before you join the account. Confirm the primary holder’s habits will help rather than harm your score. If the primary account carries high balances or past lates, being added will damage your credit instead of improving it.

Strategic account preservation and aging methods:

Dormant-account activity rotation: Set a recurring subscription or utility payment on each old card, then automate the payment to keep the account active without daily management.

Authorized-user selection criteria: Choose accounts with at least ten years of history, consistent on-time payments, and utilization below 10% to maximize the benefit.

Aging-in rules: Understand that newly opened accounts immediately lower your average age, so space out applications by at least six months when possible.

Minimizing negative age impacts from new accounts: If you must open a new card, do so only after your existing accounts have aged past the two-year mark to soften the average-age dilution.

Account-closure risk assessment: Before closing any card, calculate how much your average age will drop and whether the closure will spike your utilization by reducing available credit.

Building a High-Value Credit Mix Without Excess Accounts

Credit mix accounts for 10% of your FICO score and reflects your ability to manage different types of credit simultaneously. A strong mix typically includes multiple revolving accounts (credit cards) and at least one installment loan (mortgage, auto loan, or personal loan). Adding an installment account when your profile contains only revolving credit can produce a noticeable score lift, but opening unnecessary debt solely for mix improvement rarely makes financial sense.

Timing new installment credit matters when you’re optimizing for 800. If you already have a solid payment history and low utilization, adding a small personal loan or a credit-builder loan can round out your mix without introducing high debt levels. If you’re still recovering from past negatives or your utilization is above 30%, prioritize those issues before expanding your credit types. Lenders care more about responsible use of existing credit than a perfectly balanced portfolio.

Small installment products, such as credit-builder loans where payments go into a savings account and you receive the funds after completion, offer a low-risk way to demonstrate installment payment history. Secured credit cards require a cash deposit equal to your credit limit and help establish or rebuild revolving credit, though they don’t add to your mix if you already have unsecured cards. Evaluate whether your current profile already contains enough diversity before opening accounts that add complexity without clear score benefit.

Strategic mix-building actions:

Strategic new-account timing: Open an installment loan only when your revolving accounts are in excellent standing and your utilization is well below 30%, so the hard inquiry and new account don’t offset the mix benefit.

Avoiding inquiry clustering: Space credit applications at least six months apart unless you’re rate-shopping for a single loan type within the 14- to 45-day grouping window recognized by FICO models.

Deciding between secured cards or builder loans: Choose a secured card if you lack revolving credit. Choose a credit-builder loan if you need to establish installment history without taking on traditional debt.

Evaluating whether current mix is already optimal: If you have three or more credit cards and at least one active installment loan with strong payment history, further mix expansion likely delivers minimal score improvement compared to optimizing utilization and payment consistency.

Advanced Negative Item Resolution & Accuracy Enforcement

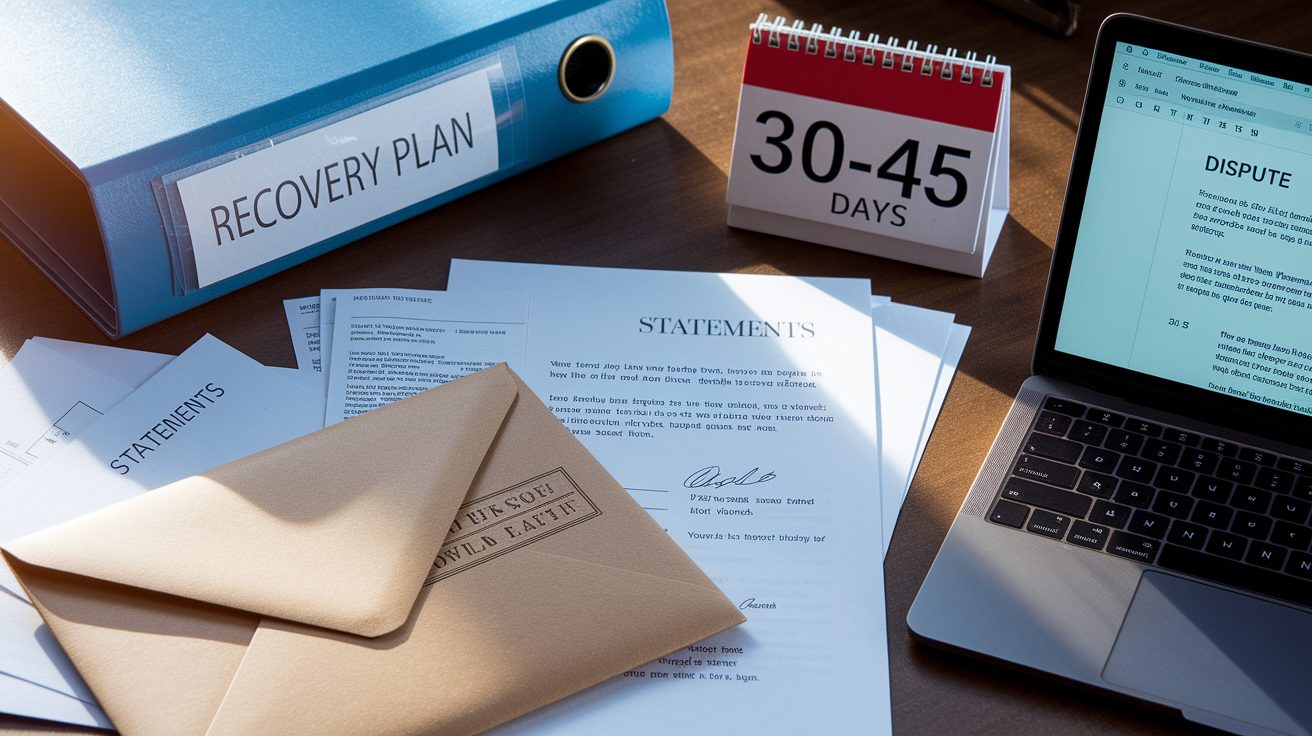

Disputing inaccurate information on your credit report triggers a formal investigation by the bureau, which must respond within 30 to 45 days. Gather documentation before filing disputes (account statements, payment receipts, settlement letters, and any correspondence with creditors) because the bureau will forward your dispute to the data furnisher, and incomplete evidence weakens your case. If the furnisher can’t verify the disputed item, the bureau must remove it, often resulting in an immediate score increase.

Escalation pathways exist when initial disputes fail. If a bureau upholds an inaccurate item after investigation, you can file a complaint with the Consumer Financial Protection Bureau or your state attorney general’s office. You can demand that the bureau include a consumer statement in your file explaining the dispute. For items that are factually correct but damaging (legitimate late payments), your options narrow to goodwill requests or waiting for the item to age off after seven years.

Strategic timing of disputes matters when you have near-term financial goals. If you’re applying for a mortgage in three months, prioritize disputes that will resolve quickly and have the largest score impact, such as incorrect late payments or accounts that don’t belong to you. Save lower-impact disputes (small balance discrepancies) for after the loan closes to avoid unnecessary bureau contact during underwriting.

| Negative Item | Time on Report | Potential Impact |

|---|---|---|

| 30-day late payment | 7 years from delinquency date | Immediate large drop; impact fades over time with clean history |

| Collection account | 7 years from original delinquency date | Severe; paying doesn’t remove it but may improve lender perception |

| Chapter 7 bankruptcy | 10 years from filing date | Catastrophic; prevents 800 score until late in the aging period |

Protecting Your Progress: Monitoring, Identity Security, and Inquiry Control

Credit monitoring tools alert you to new accounts, inquiries, and balance changes, allowing you to catch identity theft or reporting errors within days instead of months. Pull your full report from each bureau at least once per year through the official annual report service. Use rolling monitoring apps or issuer-provided score tracking for monthly updates. Monitoring doesn’t improve your score directly, but it prevents damage by catching problems early.

Hard inquiries from credit applications affect your score for 12 months and remain visible for 24 months. Rate shopping for a mortgage, auto loan, or student loan within a 14- to 45-day window groups multiple inquiries into a single impact under most FICO models, but inquiries outside that window count separately. Soft inquiries from prequalification checks, employer background screenings, or your own credit pulls don’t affect your score at all, so always ask whether a lender will use a soft or hard pull before authorizing a credit check.

A credit freeze blocks new creditors from accessing your report, preventing identity thieves from opening accounts in your name. Freezes don’t affect your score, existing accounts, or employment screenings, and you can lift a freeze temporarily when you need to apply for credit. Freezing your credit at all three bureaus offers the strongest protection against unauthorized hard inquiries and fraudulent account openings.

Key protection and inquiry-control tactics:

Proactive freeze strategy: Freeze your credit at Experian, TransUnion, and Equifax as a default state, lifting the freeze only when you initiate a credit application.

Soft-pull prequalification auditing: Use prequalification tools from multiple lenders to compare offers without triggering hard inquiries, then apply only to the best option.

Optimal rate-shopping windows: Cluster all mortgage or auto loan applications within a 14-day period to ensure FICO treats them as a single inquiry, and avoid mixing loan types during that window.

Expected Timelines for Reaching an 800 Based on Your Starting Point

Timelines for reaching an 800 credit score depend on your starting score, the severity of any negative items, and how quickly you can optimize payment history, utilization, and account age. Moving from a score in the 760 range requires only incremental improvements (lowering utilization from 20% to under 10%, adding six months of perfect payments, or allowing your average account age to mature by another year). Most people starting above 760 can reach 800 within 12 to 18 months if they maintain flawless habits and avoid new negative items.

Starting from the low 700s, expect 18 to 36 months of consistent behavior. You likely have a few small negatives aging off, moderate utilization, or a thin credit file that needs more depth. Focus on driving utilization below 10%, keeping every payment on time, and avoiding new inquiries while your existing accounts mature. If you have a single late payment from two years ago, its impact will fade as you build more clean months, but reaching 800 will take longer if the late occurred recently.

Rebuilding from the 600s typically requires two to five years. Scores in this range often carry collections, multiple late payments, or high utilization. You need to clear or settle collections, pay down balances aggressively, and demonstrate at least two years of spotless payment behavior before FICO models will push you into the 800 tier. Adding new positive accounts through secured cards or credit-builder loans can help, but only after you’ve stabilized your existing accounts.

Recovery from scores below 600 demands patience and often takes five to seven years or more, especially if your report includes bankruptcy, foreclosure, or multiple charge-offs. Major negatives remain visible for seven to ten years, and their impact diminishes slowly. During the early years, focus on rebuilding payment history and keeping utilization near zero. As negative items age past the three- to five-year mark, their weight lessens, and your score will begin climbing faster if your recent behavior is strong.

Timeline paths based on starting score:

760 and above: 12 to 18 months with optimized utilization, zero new negatives, and steady account aging.

Low 700s (700 to 740): 18 to 36 months, requiring sustained low utilization, perfect payments, and some account maturation.

600s (600 to 699): Two to five years, depending on the number and recency of negative items and how quickly you can pay down debt and build clean payment history.

Below 600: Five to seven years or longer, particularly if major negatives like bankruptcy or foreclosure are present. Score gains accelerate as negatives age beyond the five-year mark.

High-Risk Behaviors That Block Progress to an 800 Score

Closing credit cards reduces your available credit and shortens your credit history, both of which can cause immediate score drops. Even if you no longer use a card, keeping it open with a small recurring charge preserves your utilization ratio and maintains your average account age. Closing your oldest card removes years of history from your profile. FICO recalculates your average age without that account, often resulting in a 10- to 30-point drop depending on how many other accounts you hold.

Utilization spikes from large purchases or reduced credit limits can erase months of score progress in a single reporting cycle. Maxing out a card, even temporarily, signals financial stress to FICO models and can drop your score by 50 points or more if your overall utilization jumps above 50%. Avoid using more than 30% of any single card’s limit. Pay down balances immediately after large purchases to prevent the high balance from being reported.

Applying for multiple new accounts within a short period clusters hard inquiries and adds several new tradelines that lower your average account age. Each hard inquiry can reduce your score by a few points. The combined effect of multiple inquiries plus new accounts can cause a drop of 20 to 40 points. Space out credit applications by at least six months unless you’re rate shopping for a single loan type within the allowable grouping window.

High-risk mistakes to avoid:

Closing old credit cards, especially your oldest account, which shortens your credit history and reduces available credit.

Letting utilization spike above 30% on any individual card or across your total revolving credit, even if you plan to pay it off the following month.

Missing a single payment, since payment history is 35% of your score and one late can cause a drop of 50 to 100 points depending on your starting score.

Opening multiple new accounts within a few months, which triggers hard inquiries and dilutes your average account age.

Ignoring credit report errors, since inaccurate late payments or accounts can linger for years if you don’t dispute them.

Co-signing loans for high-risk borrowers, because their missed payments appear on your report and damage your score even though you’re not the primary borrower.

Final Words

Pull your credit reports, set up automatic payments, and cut reported balances before statement close. If you can do one thing, automate on-time payments first.

This post gave a quick playbook: the five score factors, fast wins for payment history and utilization, accuracy checks and dispute steps, advanced tactics for utilization and account age, plus timelines and common mistakes to avoid.

Use this plan as your playbook for how to get 800 credit score, start small, track progress, and protect your reports. You’ll get there with steady habits and patience.

FAQ

Q: How hard is it to get an 800 credit score?

A: Getting an 800 credit score is hard but achievable; it usually takes several years of perfect payment history, utilization below about 10%, long-standing accounts, and no recent negatives on your report.

Q: What credit score do you need for a $400,000 house?

A: The credit score you need for a $400,000 house depends on loan type and lender; aim for at least 620 for conventional loans, 740+ for best rates, and higher scores cut your interest and down payment needs.

Q: What can a 900 credit score get you?

A: A 900 credit score isn’t possible; FICO and Vantage stop at 850. An 850 score earns the lowest rates, easiest approvals, highest credit limits, and best credit-card offers.

Q: How to get 800 credit score in 45 days?

A: Getting an 800 credit score in 45 days is unlikely unless you’re already near 800; focus on fixing report errors, lowering reported balances before statement close, and automating on-time payments.