{kind=link}

Think putting everything into one hot stock is smart?

That’s a risky bet that can wipe out years of progress.

A diversified portfolio spreads your money across different asset types, like stocks, bonds, real estate, and cash, so one bad holding doesn’t control your outcome.

It doesn’t promise big overnight wins, but it often delivers steadier growth and fewer brutal drops over time.

If you only do one thing today, pick low-cost index funds that cover many companies and add a bond fund to match how much volatility you can sleep through.

Core Explanation of a Diversified Portfolio

A diversified portfolio spreads your investments across different types of assets, industries, and geographies so that no single holding controls your financial outcome. Instead of betting everything on one company or sector, you split your money among stocks, bonds, real estate, and other investments that don’t all move in the same direction at the same time. The core idea is simple: don’t put all your eggs in one basket.

When you own only one stock and that company stumbles, your entire portfolio takes the hit. Diversification cuts that concentrated risk by making sure each investment represents just a slice of your total holdings. If one asset drops, others may hold steady or even gain, cushioning the overall impact.

This approach balances growth potential with downside protection. You give up the chance to double your money overnight on a single hot stock, but you also avoid losing everything if that bet goes wrong. Here’s what a diversified mix might look like:

Stocks in multiple companies and sectors for growth potential.

Bonds that generate interest income and stabilize during stock market drops.

Real estate to protect against inflation and add rental income.

Cash or cash equivalents for quick access and emergency needs.

Why Diversification Reduces Risk

Diversification works because different assets react differently to the same economic events. When stocks fall during a recession, bonds often rise as investors seek safety and central banks cut interest rates. When inflation heats up, real estate and commodities may gain value while bonds lose purchasing power. By holding uncorrelated assets, you smooth out the wild swings any single investment might experience.

This smoothing effect is the core mechanic of risk reduction. A portfolio split between stocks and bonds will typically see smaller drops during market crashes than a stock only portfolio, because the bond portion acts as a shock absorber. You won’t capture every upside move in the hottest sector. But you also won’t suffer the full downside when that sector corrects. Over time, this steadier path can produce more consistent returns and fewer sleepless nights.

Real world examples show the difference. During the 2008 financial crisis, a diversified portfolio holding stocks, bonds, and some alternative assets lost less and recovered faster than a concentrated portfolio of bank stocks. In the 2022 bear market, portfolios with inflation protected bonds and commodities held up better than those in pure tech equities. Diversification doesn’t guarantee profit or prevent all losses, but it limits how much damage any single event can do.

Major Asset Classes in a Diversified Portfolio

A diversified portfolio draws from several major asset classes. Each serves a distinct purpose and reacts differently to economic shifts. Understanding what each class offers helps you build a balanced mix that fits your goals and risk tolerance.

Stocks

Stocks represent ownership in companies and offer the highest growth potential over the long term. They’re also the most volatile, swinging sharply based on earnings reports, economic news, and investor sentiment. In a diversified portfolio, stocks provide the engine for wealth building, especially when you have years or decades before you need the money. A mix of large cap stalwarts, mid cap growth companies, and small cap opportunities spreads risk within the stock portion itself.

Bonds

Bonds are loans you make to governments or corporations in exchange for regular interest payments and the return of your principal at maturity. They generate predictable income and tend to be less volatile than stocks. When stock markets tumble, bonds often hold steady or even appreciate as investors shift to safer assets. Including bonds in your portfolio acts as a counterbalance, reducing overall swings and providing cash flow through interest payments.

Real Estate

Real estate investments, whether through physical properties or real estate investment trusts (REITs), offer protection against inflation and the potential for rental income. Property values and rents tend to rise when consumer prices climb, preserving purchasing power. Real estate often moves independently of stocks and bonds, adding another layer of diversification. It can be less liquid than stocks or bonds, so it’s typically a smaller slice of a diversified portfolio.

Commodities

Commodities, such as oil, gold, agricultural products, and industrial metals, respond to global supply and demand dynamics rather than corporate earnings or interest rates. They can protect against inflation and geopolitical risk. When inflation surges, commodity prices often jump, offsetting losses elsewhere. Commodities are sensitive to factors like weather, trade policies, and global economic growth, making them a distinct and sometimes volatile addition to a diversified mix.

Together, these asset classes provide a foundation that balances growth, income, stability, and inflation protection. No single class dominates your returns or your losses, and each plays a specific role depending on market conditions.

Simple Steps to Build a Diversified Portfolio

Building a diversified portfolio doesn’t require exotic investments or a finance degree. Start by mapping out what you’re trying to accomplish and how much volatility you can stomach, then allocate your money across asset classes in a way that matches those answers.

Determine your risk tolerance. If a 20% drop would keep you awake at night, lean heavier on bonds and cash. If you can ride out downturns for years, you can carry more stocks.

Choose your asset mix. Decide what percentage goes to stocks, bonds, real estate, and cash based on your timeline and goals. Younger investors with decades ahead often hold more stocks. Retirees typically hold more bonds.

Select diversified funds. Instead of picking individual stocks or bonds, use broad index funds or ETFs that hold hundreds or thousands of securities. One S&P 500 index fund instantly diversifies you across 500 large U.S. companies.

Rebalance annually. Over time, winners grow and losers shrink, throwing your original allocation off balance. Once a year, sell a bit of what’s grown and buy what’s lagged to restore your target percentages.

Review your goals regularly. Life changes, markets shift, and your risk tolerance may evolve. Check in at least once a year to make sure your portfolio still fits where you’re headed.

Beginners often start with a three fund portfolio: a U.S. stock index fund, an international stock index fund, and a bond index fund. This simple setup delivers broad diversification without requiring you to research individual companies or time the market. As you learn more, you can add real estate, commodities, or sector specific funds, but the core principle stays the same. Spread your dollars so no single bet determines your outcome.

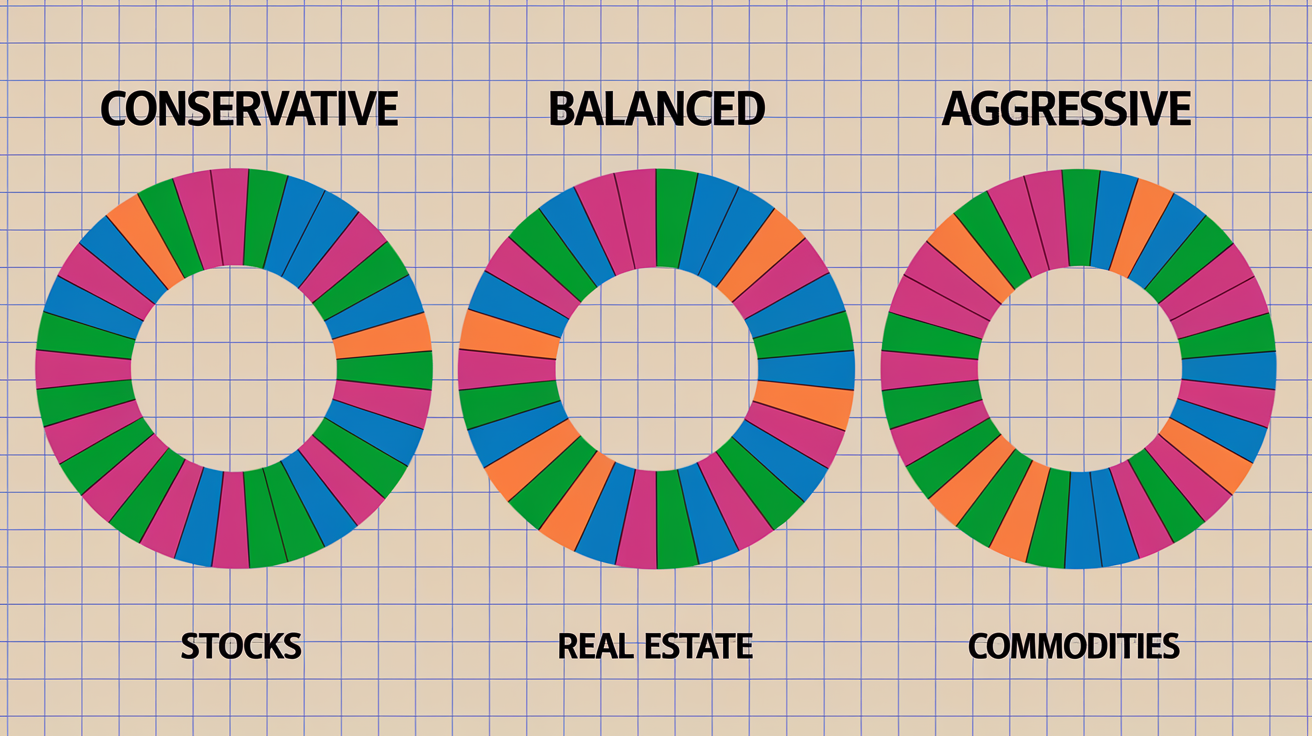

Examples of Diversified Portfolio Allocations

What diversification looks like in practice depends on how much risk you’re willing to take and how soon you need the money. Below are three common models that show how different investors might split their holdings.

| Risk Level | Stocks | Bonds | Real Estate | Commodities | Cash |

|---|---|---|---|---|---|

| Conservative | 30% | 50% | 10% | 5% | 5% |

| Balanced | 60% | 30% | 5% | 3% | 2% |

| Aggressive | 80% | 10% | 5% | 3% | 2% |

These examples aren’t one size fits all rules. A conservative portfolio prioritizes capital preservation and steady income, making it suitable for retirees or anyone who can’t afford large losses. A balanced portfolio splits the difference, offering growth potential with meaningful downside cushioning for mid career savers. An aggressive portfolio chases higher returns by leaning heavily on stocks, accepting bigger swings in exchange for long term growth, and works best for young investors with decades to recover from downturns. Your actual allocation should reflect your timeline, income needs, and how you react when markets drop.

Final Words

Put this into practice: you now have a clear definition of diversification and why spreading holdings reduces risk. The post walked through the main asset classes—stocks, bonds, real estate, commodities—offered simple steps to build a plan, and showed sample allocations to match different goals.

If you’re still asking what is a diversified portfolio, it’s a mix of different assets that smooths ups and downs so one loss won’t derail your progress. Start small, rebalance regularly, and you’ll see steadier results over time.

FAQ

Q: What is an example of a diversified portfolio?

A: An example of a diversified portfolio is 60% stocks, 30% bonds, 5% real estate (REITs), and 5% cash — combining growth, income, inflation protection, and short-term safety.

Q: How much is $1000 a month invested for 30 years?

A: The value of $1,000 a month invested for 30 years depends on return; at 6% it’s about $1.0M, at 7% about $1.22M, and at 8% about $1.49M.

Q: How many stocks for a diversified portfolio?

A: The number of stocks for a diversified portfolio is typically 20–30 individual stocks to reduce single-stock risk, or use 3–6 broad ETFs for similar diversification more simply.

Q: How to diversify portfolio for 2026?

A: To diversify a portfolio for 2026, use broad global stock ETFs, add bonds for income, include real estate or commodities for inflation protection, set a clear allocation, and rebalance annually.