{kind=link}

You don’t need more willpower to stop impulse buying online.

You need quick ways to break the buy-now loop before you tap Place Order.

Most impulsive buys start at night, on your phone, after one targeted ad.

This post gives seven smart tactics you can use right away, fast fixes, habit changes, and money rules that actually work.

If you want one fast move today, pick one.

Close the app, set a 10-minute timer, or check your real bank balance.

Use the rest of the tactics to build new habits.

Ultra-Fast Actions to Immediately Halt Online Impulse Buying

When you catch yourself mid-impulse, seconds matter. Most online impulse buying happens late at night on mobile devices, triggered by boredom or a targeted ad that pops up while you’re scrolling. The dopamine cycle starts the moment you tap “Add to Cart,” and the only way to stop it is to interrupt the chain immediately.

You don’t need a system or a plan in that moment. You need a fast intervention that breaks the loop before you hit “Place Order.” The goal is to put physical or mental distance between you and the purchase screen, giving your brain a chance to shift out of impulse mode.

-

Open your banking app and check your account balance. Seeing your real balance instead of an abstract number interrupts the fantasy. “I just got paid 2 days ago and I’m down to $340? Wait.”

-

Close the browser tab or shopping app completely. If it’s out of sight, the urgency fades. Don’t minimize it. Close it.

-

Set a timer for 10 minutes and step away from your device. Walk to another room, get water, or do anything that’s not looking at a screen.

-

Turn off your Wi-Fi or disable mobile data temporarily. This creates a hard stop. You can’t buy if you can’t load the checkout page.

-

Uninstall the shopping app from your phone if you use it more than twice a week. The friction of reinstalling and re-logging makes impulse buying much harder.

Managing Online Shopping Habits to Reduce Impulsive Purchases

Your inbox and social feeds are designed to create urgency. Retailers send new releases weekly, sometimes daily, with subject lines like “Just Dropped” or “Only 3 Left.” Every notification is a nudge toward impulse buying online, and the more exposure you have, the more often you’ll be tempted.

The fix is to reduce the volume and visibility of these triggers. Create an email rule that automatically moves all retailer emails into a folder named “Shopping” so they never hit your main inbox. If you want to go further, set those promotional emails to auto-delete after 30 days so you’re not tempted to browse old sale announcements. Some people unsubscribe entirely from marketing lists, which works if you can commit to it. If you still want occasional deals, set up a separate email account just for retailer sign-ups. One writer reports having “thousands of unread emails” in a shopping-only inbox and emptying it roughly twice a year. Out of sight, out of mind.

Social media amplifies impulse purchases because influencers, ads, and even friends create spending pressure. Reduce screen time on platforms where you see the most shopping content. Unfollow accounts that constantly promote products or “haul” videos. Turn off push notifications from shopping apps so you’re not pinged every time there’s a flash sale or restocked item.

Create email filters to move retailer messages into a dedicated folder. Unsubscribe from promotional emails or set them to auto-delete after 30 days. Use a separate “junk” email for shopping sign-ups and check it only when you need a specific coupon. Mute push notifications from all shopping apps and unfollow high-spend accounts on social media.

Payment Friction Techniques to Stop Impulse Buying Online

Saved payment methods make buying too easy. When your credit card is already stored and autofill is enabled, you can complete a purchase in under 10 seconds. That speed is the enemy of thoughtful spending.

Remove all saved payment information from retailer websites and apps. Delete stored cards from Amazon, Target, and anywhere else you shop frequently. Disable Amazon 1-Click entirely. It’s designed to eliminate decision time, which is exactly what you need more of. Turn off browser autofill for payment fields so you have to manually enter your card number, expiration date, and CVV every time. The extra 60 seconds gives your brain a chance to ask, “Do I actually need this?”

| Method | How It Helps | Effort Level |

|---|---|---|

| Remove saved credit cards from retailer accounts | Forces manual entry; adds 30–60 seconds to checkout | Low (one-time setup) |

| Disable browser autofill for payment fields | Requires typing card details each time | Low (browser settings change) |

| Turn off Amazon 1-Click and similar features | Eliminates instant-purchase options | Very Low (account settings toggle) |

Psychological Triggers Behind Impulse Buying Online

Impulse purchases almost always serve an emotional need, not a functional one. You’re not buying because you need the item. You’re buying because you’re stressed, bored, celebrating, or feeling low, and shopping offers a quick dopamine hit.

Emotional Triggers

Four emotional states drive most impulse buying online: stress, happiness, sadness, and boredom. Stress shopping happens when you’re overwhelmed and want a distraction or a sense of control. Happiness shopping is reward-seeking. “I had a good day, I deserve this.” Sadness shopping is self-soothing, trying to fill an emotional gap. Boredom shopping is the most common and happens when you’re passively scrolling with no real goal.

Situational Triggers

Three situational factors amplify emotional triggers: sales and discounts, targeted advertisements, and peer influence. A “40% off” banner creates urgency even when you weren’t planning to buy. Retargeted ads follow you across the web, reminding you of items you looked at once. Friends or influencers posting hauls or “must-haves” create social pressure to keep up.

The fix starts with awareness. When you feel the urge to shop, pause and ask: “What am I actually feeling right now?” If the answer is bored, stressed, or sad, the purchase won’t solve it. You’ll feel better for a few minutes, then you’ll feel worse when the package arrives and you realize you didn’t need it.

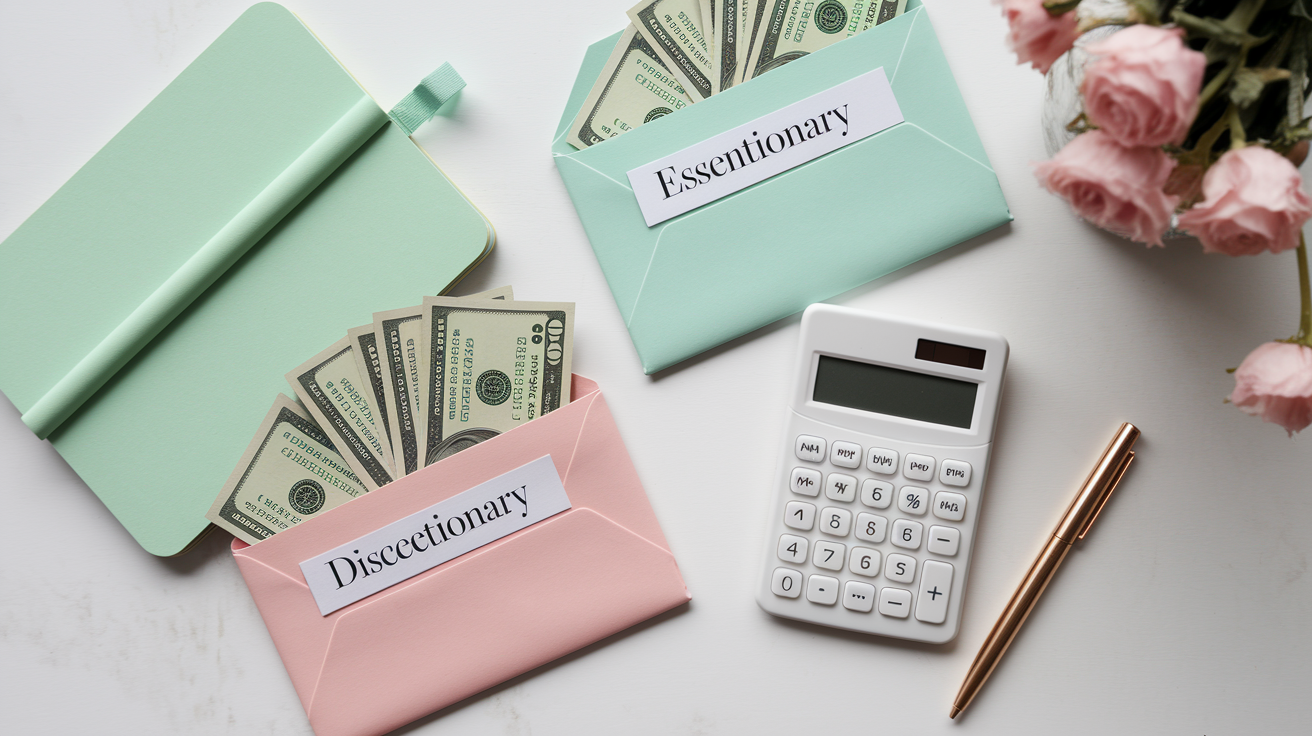

Budget-Based Approaches to Control Impulse Buying Online

A budget without room for discretionary spending doesn’t work because it feels like deprivation. You’ll rebel against it the moment something catches your eye. The solution is to separate your money into two clear categories: Essentials and Discretionary.

Essentials cover rent, groceries, bills, and savings. Discretionary covers entertainment, dining out, and shopping. If you allocate $250 per month for discretionary spending, you can buy what you want within that limit without guilt. The key is tracking against that number. When you hit $250, you stop until next month. If you go over, you see it immediately and adjust.

Structuring a Practical Discretionary Budget

Start by reviewing your last two months of credit card and bank statements. Highlight every purchase that wasn’t essential. Add up the total, then divide by two to get your average monthly discretionary spend. If that number is $400 and you want to curb impulse purchases, set your new monthly limit at $250 or $300. Build in a small buffer for the occasional planned splurge, like a birthday gift or concert tickets.

Set a weekly spending cap (example: $60 per week if your monthly limit is $250). Fund your discretionary account or envelope at the start of each month so you see the full amount. Use a budgeting app that sends alerts when you’re close to your limit. Set up automatic transfers to savings on payday so discretionary money is what’s left, not an afterthought. Review your spending every Sunday to see where you are for the week.

Delayed Gratification Systems for Online Shopping Control

Waiting breaks the impulse. The standard rule is a 24-hour delay for any non-essential purchase. If you still want the item tomorrow, buy it. If you forget about it, you didn’t need it.

For bigger purchases or when you’re trying to curb impulse buying more aggressively, extend the wait to 48 hours or even a full week. Let items sit in your cart for a few days. Most retailers send reminders or discount codes within 48 hours when they see an abandoned cart, so waiting often saves you money too. One common pattern: you add something on Monday, and by Wednesday the retailer emails you a “special offer” for 15% off or free shipping.

Use saved-for-later features and wishlists to organize your intentions. Create three categories: Essentials (things you truly need soon), Wants (nice-to-haves with no urgency), and Long-term Desires (aspirational or expensive items). Review these lists weekly and prune anything that no longer feels necessary. If an item stays in “Wants” for a month without moving to “Essentials,” you probably don’t need it.

Precommitment strategies also help. Decide in advance: “I won’t buy clothing unless I’ve reviewed my closet first,” or “I won’t buy electronics unless I’ve compared prices on at least two other sites.” These rules create automatic checkpoints that slow you down.

Implement a 24-hour rule for all non-essential purchases. If you still want it tomorrow, revisit the decision. Use a 30-day rule for purchases over $100. Add the item to a wishlist and wait a full month before buying. Let items sit in your cart for at least 48 hours and check if the retailer sends a discount code. Organize saved items into Essentials, Wants, and Long-term Desires, then review and prune weekly.

Tools and Technology to Stop Impulse Buying Online

Browser extensions and apps can automate friction and reduce exposure to impulse triggers. Ad blockers eliminate retargeted ads that follow you around the web after you view a product once. Website blockers let you blacklist specific retail sites during certain hours, for example, blocking Amazon between 8 p.m. and 8 a.m. when late-night boredom shopping is most likely.

Price comparison extensions force you to pause and check if you’re getting a good deal, which interrupts the “buy now” reflex. Coupon finders do the same thing. They add a 10-second delay while searching for discount codes, giving you time to reconsider. Budget-tracking apps like Mint or YNAB flag overspending in real time, so you see immediately when a purchase pushes you over your discretionary limit.

Install an ad blocker to eliminate retargeted shopping ads and reduce impulse triggers. Use a website blocker to restrict access to your most-shopped stores during high-risk hours. Add a price comparison or coupon extension that forces a brief pause at checkout.

Behavior Replacement Techniques to Prevent Emotional Online Spending

When the urge to shop hits, your brain is looking for a dopamine hit or a distraction. If you don’t offer an alternative, the urge will win. The goal is to interrupt the cycle by substituting a different activity that satisfies the same emotional need.

If you’re bored, close the shopping app and read a chapter of a book, take a 10-minute walk, or play with your kids. If you’re stressed, try a five-minute breathing exercise or call a friend instead of scrolling through sale pages. If you’re feeling low and want a pick-me-up, make a cup of tea, listen to a favorite song, or do something small that feels good without costing money. These alternatives weaken the automatic “I’m bored, so I’ll shop” loop by rewiring the habit over time.

Long-Term Habits to Break Online Impulse Buying

Stopping impulse buying permanently requires building new default behaviors. One effective method is implementation intentions, which are “if-then” plans you set in advance. For example: “If I feel like buying something online, then I’ll check my bank balance first.” Or: “If I open a shopping app out of boredom, then I’ll close it and text a friend instead.” These precommitted rules reduce decision fatigue because you’ve already decided what to do when the urge hits.

Pause-and-reflect routines help too. Before any purchase, ask yourself: “Do I already own something similar? Will I use this more than once? Have I checked for a coupon or a cheaper option?” These questions slow down automatic buying and force intentional decisions. Value-based spending is another long-term strategy. List your top three personal values, maybe family, health, and financial security, and ask whether each purchase aligns with at least one of them. If it doesn’t, skip it.

Monthly spending audits keep you accountable. At the end of each month, review your credit card and bank statements. Highlight every impulse purchase. Add up the total. If you spent $180 on impulse buys in March, set a goal to reduce it to $120 in April. Track your progress over time and celebrate the months when you stay within your discretionary budget.

Monthly Spending Audit Method

Set a recurring calendar reminder for the last Sunday of each month. Pull up your bank and credit card statements and highlight every purchase that wasn’t planned or budgeted. Sort them into categories: clothing, electronics, food delivery, subscription impulse-adds. Calculate the total for each category and for all impulse purchases combined.

Compare this month’s total to last month. If it went down, note what worked. If it went up, identify the specific trigger. Maybe you were stressed that week, or a favorite store had a sale. Adjust your email filters, spending limits, or behavior-replacement strategies based on what you learn. Over time, this audit becomes a feedback loop that helps you spot patterns and refine your approach.

Final Words

In the action, you learned ultra-fast interrupts, like closing the app, checking your balance, and stepping away, and longer fixes such as email filters, removing saved cards, delay rules, budgeting, tools, and habit tricks to cut emotional buys.

Pick one small change to start. Uninstall a shopping app, set a 24-hour rule, or turn off push notifications. Track results with a quick monthly check.

Try the 10-minute pause as your next move. That simple habit helps show how to stop impulse buying online and builds steady control.

FAQ

Q: How can impulse buying be prevented?

A: Impulse buying can be prevented by quick moves: close the app, check your balance, step away for 10–30 minutes, remove saved payment methods, or use a 24‑hour waiting rule.

Q: What is the 1 rule for impulse buys?

A: The one rule for impulse buys is to wait at least 24 hours before buying nonessentials; if you still want it and it fits your discretionary budget, then purchase.

Q: Is impulse buying part of ADHD?

A: Impulse buying can be part of ADHD because impulsivity and reward‑seeking raise quick purchases; talk to a clinician and use friction, budgets, and delay rules to reduce harm.

Q: Why am I obsessed with online shopping?

A: Being obsessed with online shopping is often caused by boredom, stress, targeted ads, and instant rewards; identify triggers, set blockers or delay rules, and replace shopping with a short alternative activity.