{kind=link}

Think debt consolidation is a one-click fix? Lenders disagree.

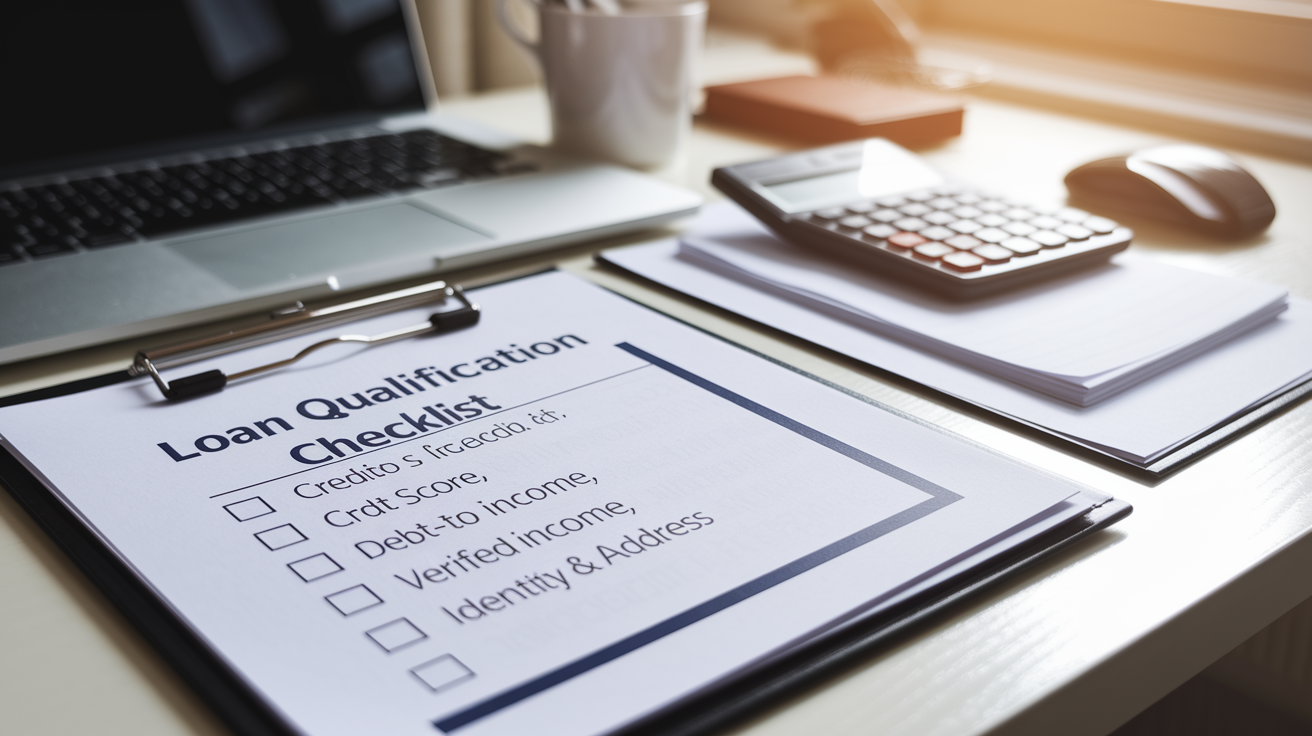

To qualify for a debt consolidation loan lenders mainly check your credit score, your debt-to-income ratio (how much of your pay goes to debt), verified income, job stability, and paperwork.

Most standard lenders look for a credit score near 650 and a DTI under about 40 percent, though options exist on either side.

This post breaks down each requirement, shows simple steps you can take now to improve your chances, and gives a quick decision rule so you know what to do next.

Key Requirements to Qualify for a Debt Consolidation Loan

Lenders want to know one thing: will you pay this back? Every application gets screened through the same basics—your credit score, how much debt you’re already carrying versus what you earn, proof you actually make the money you say you do, and whether you’ve held a job long enough to count on that income next month. These checks help predict if you can handle a single fixed payment without missing it. When you know what they’re looking for, you can pull together the right paperwork and shore up weak spots before hitting submit.

Most lenders want a credit score around 650 at minimum. Some will go lower, but you’ll pay for it with a higher rate. Your debt-to-income ratio—the slice of your gross monthly pay that already goes to debt—should usually stay under 40 percent. Say you bring in $5,000 a month and $2,000 goes to debt payments. That’s 40 percent. Lenders also need recent pay stubs or tax returns to verify your income, plus a work history showing you’ve been in your current job or field for about two years. Freelancers and gig workers can get approved if they can document steady earnings.

Documentation is simple but you can’t skip it. Expect to hand over pay stubs from the last 30 days, your latest tax return, proof of any side income, a government ID, proof of address like a utility bill or lease, and bank statements. Some lenders use secure read-only tools to check your income and account balances directly, which can get you funded in as little as one business day once everything’s in.

Five primary things lenders check:

- Credit score and what’s on your credit report

- Debt-to-income ratio (monthly debt divided by gross monthly income)

- Verified income from pay stubs, tax returns, or bank deposits

- Job stability and how long you’ve been in your current role or industry

- Documents proving who you are, where you live, and that you own the bank account

Credit Score Requirements for Debt Consolidation Approval

Your credit score drives whether you get approved and what you’ll pay in interest. Lenders lean on FICO scoring models most of the time, though some check VantageScore too. A score near 650 is a common floor for standard personal loans, but the best rates usually go to people above 740. If you’re below 650, you can still find options, but APRs climb into the mid-twenties or higher. A hard inquiry when you formally apply might drop your score about five points, so it makes sense to prequalify with a soft pull first.

Interest rates jump around a lot depending on your score. Borrowers with excellent credit—780 or higher—might see APRs near 9 percent, sometimes even lower for really short terms. Fair credit in the mid-600s often lands you somewhere between 15 and 20 percent. Poor credit below 580 can push APRs to 28 percent or more, which might wipe out any savings compared to your current credit card balances. If your score’s on the edge, raising it even 30 or 40 points before you apply can shave several percentage points off your APR and save you hundreds or thousands over the loan’s life.

| Score Range | Likelihood of Approval | Typical APR Range |

|---|---|---|

| 740+ | High | ~9% to 14% |

| 650–739 | Moderate to High | ~15% to 22% |

| Below 650 | Lower; Limited Options | ~23% to 35%+ |

Debt-to-Income Ratio Standards for Consolidation Loan Approval

Your debt-to-income ratio shows lenders what percentage of your monthly income already disappears into debt. Calculate it by adding up all your monthly debt payments—credit cards, car loans, student loans, any other installment debt—then divide by your gross monthly income and multiply by 100. Earn $5,000 a month and owe $2,000 in payments? That’s 40 percent. Most lenders want to see DTI below 40 percent. Some draw a hard line at 43 or 45 percent. High DTI is one of the top reasons applications get rejected.

If your DTI sits above what lenders want, you’ve got options. Paying down existing balances—even a couple hundred dollars—lowers your monthly minimums and improves the ratio. Boosting your income works too, whether through a raise, more hours, or side work you can document. Some people consolidate part of their debt to bring DTI into range, then apply for a bigger loan later once the ratio drops. The point is showing lenders you have room in your budget to handle one more fixed payment without stretching too thin.

Four steps to cut your DTI before applying:

- Make extra payments on high-interest credit cards to drop your monthly minimums.

- Don’t take on new debt or open new credit accounts while you’re getting ready to apply.

- Document and report any extra income—side gigs, freelance work, rental income—that you can back up with bank deposits or tax forms.

- Work with a nonprofit credit counselor to build a paydown plan targeting your highest-rate or highest-payment debts first.

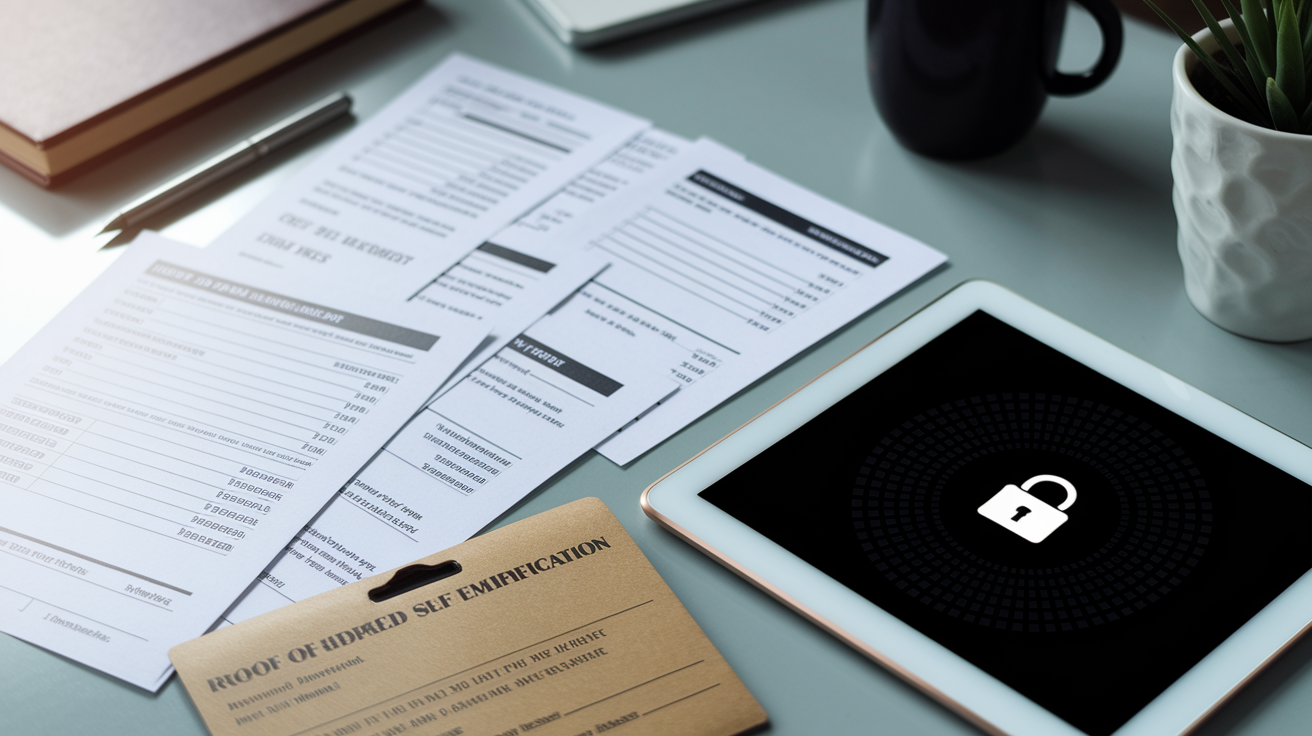

Income Verification and Documents Needed to Qualify

Lenders need proof you earn enough to cover the new loan payment, your other debts, and your day-to-day expenses. That means rounding up recent pay stubs—usually the last two or three—plus your most recent tax return if you’re employed. Self-employed people, freelancers, and gig workers typically submit one or two years of tax returns (1040 with Schedule C or 1099 forms) to show consistent income. Some lenders also look at bank statements showing regular deposits, especially if your income bounces around month to month.

You’ll also provide documents confirming your identity, address, and bank account. A driver’s license, passport, or state ID covers identity. Proof of address can be a recent utility bill, lease, bank statement, or voter-registration card. For your bank account, expect to share a recent statement or grant the lender secure read-only access through something like Plaid. This lets them verify your account balance and sometimes your income deposits in real time, which can speed approval and funding. If you submit everything fast and complete, some lenders fund within one business day.

If you earn income from multiple sources—W-2 job plus freelance work, for instance—document all of it. Lenders count side income as long as you can prove it’s steady. That usually means at least six months to a year of consistent deposits or a 1099 on your tax return. The more you provide upfront, the faster underwriting moves and the fewer follow-up requests you’ll see.

Six documents usually required:

- Recent pay stubs (last 30 days, sometimes last 60)

- Most recent tax return (1040, plus schedules if self-employed)

- Government-issued photo ID (driver’s license, passport, state ID)

- Proof of address (utility bill, lease, bank or credit card statement)

- Bank account statement or secure account connection for verification

- Proof of additional income (1099 forms, side-gig deposits, rental agreements)

Types of Debt Consolidation Loans and Their Qualification Rules

Debt consolidation loans split into two main types: unsecured personal loans and secured loans backed by collateral. Unsecured personal loans are more common. You don’t pledge an asset, so approval hinges almost entirely on credit score, income, and DTI. Rates for unsecured loans typically range from about 9 percent for excellent credit to 28 percent or higher for fair or poor credit. Terms usually run two to five years, though some lenders stretch to seven. No collateral means lenders offset risk by charging higher rates to lower-credit borrowers and keeping loan amounts moderate—often $1,000 to $50,000, sometimes up to $100,000 for the strongest profiles.

Secured consolidation loans use an asset as collateral, usually your home. Home equity loans and home equity lines of credit fall here. Because your property backs the loan, lenders can offer lower interest rates—sometimes several points below unsecured personal loans—and longer terms, in some cases up to 30 years. That can make monthly payments easier to handle. But the tradeoff is serious: default and the lender can foreclose on your home. Secured loans also require enough equity in your property. Lenders typically look at loan-to-value ratios and prefer to keep combined LTV below 80 or 85 percent, meaning your total mortgage debt plus the new loan shouldn’t top 80 to 85 percent of your home’s appraised value.

Choosing between unsecured and secured depends on your credit, your equity, and how much risk you’re willing to take. Solid credit and want fast funding without risking your home? Unsecured personal loan. Own a home, have substantial equity, and need a lower rate or bigger loan amount? Home equity product can work—just be certain you can make every payment. Losing your house isn’t theoretical. It’s a real consequence of secured-loan default.

Unsecured Personal Consolidation Loans

Unsecured personal loans don’t require collateral, so your credit score and income carry all the weight. Lenders typically want scores above 650 for competitive rates, though some specialize in fair or even poor credit lending at higher APRs. Terms are fixed—same payment every month until it’s paid off—and most loans close within a few days once you submit documentation. Origination fees can range from 1 to 12 percent, often deducted from what you receive, so factor that into your net proceeds. No collateral means faster approvals and less paperwork, but higher rates for weaker credit.

Home Equity Loans

A home equity loan is a second mortgage that pays out a lump sum you can use to consolidate debt. Interest rates generally run lower than unsecured personal loans because your home secures the debt. You’ll need a credit score typically above 620, enough equity (many lenders want at least 15 to 20 percent equity remaining after the loan), and proof of income and employment. Terms can stretch to 30 years, which lowers monthly payments but increases total interest. Closing costs—appraisal, title search, origination—can add up to a few thousand dollars, so home equity loans make sense for larger consolidation amounts where the rate savings justify the upfront cost and the risk.

HELOCs

A home equity line of credit works like a credit card secured by your home. You’re approved for a maximum credit line and draw what you need during a draw period (often 10 years), paying interest only on what you use. After the draw period ends, you enter repayment, where you pay back principal and interest. HELOCs often have variable interest rates, so your payment can shift as market rates move. Qualification is similar to a home equity loan—good credit, verified income, sufficient equity—but HELOCs offer more flexibility if you want to consolidate debt over time or keep a reserve for future expenses. The variable-rate risk and secured nature mean you need stable income and a clear repayment plan before tapping home equity this way.

How Lenders Underwrite a Debt Consolidation Loan Application

Underwriting is how lenders decide whether to approve you, how much to lend, and what interest rate to charge. It starts with prequalification, which uses a soft credit pull and basic income information to estimate your likely rate and loan amount. Prequalification doesn’t guarantee approval, but it lets you shop offers without hitting your credit score. Once you pick a lender and submit a formal application, a hard inquiry shows up on your credit report. That hard pull gives the lender access to your full credit history, including payment patterns, account ages, and any negative marks like late payments, collections, or charge-offs.

During underwriting, the lender verifies everything you provided—income through pay stubs or tax returns, employment through a call to your employer or review of your work history, and bank account through statements or secure connection. They calculate your DTI, review your credit report for red flags, and assess whether the loan amount and term fit your profile. If everything checks out, they issue approval with a final APR, loan amount, and repayment term. If something raises concern—high DTI, recent missed payments, income that doesn’t match what you stated—they may ask for more documentation, offer a smaller loan, or deny the application.

Underwriting timelines vary. Some online lenders use automated systems that approve or deny within minutes. Others take a few business days, especially if you’re self-employed or your income sources are complex. Fast document submission speeds things up. Upload clear, complete pay stubs and tax returns right away and you’re more likely to get funded within one to three days.

Four lender red flags that can slow or stop approval:

- Debt-to-income ratio above the lender’s cutoff (commonly 40 to 45 percent)

- Recent late payments or delinquencies in the past 12 months

- Unstable or unverifiable income (frequent job changes, employment gaps, inconsistent deposits)

- Outstanding collections, charge-offs, or a bankruptcy within the past few years

Actions to Improve Your Chances of Qualifying for a Consolidation Loan

If you don’t quite meet lender thresholds today, a few targeted moves over the next few months can shift the odds. Start with your credit score. Payment history makes up 35 percent of your FICO score, so set up automatic payments or reminders so you never miss a due date. Credit utilization—how much of your available credit you’re using—accounts for another 30 percent. Pay down credit card balances, even by a few hundred dollars, and you can lift your score within one billing cycle. If you find errors on your credit report—accounts that aren’t yours, wrong balances, or late payments you made on time—dispute them with the credit bureau. Corrections can take 30 days but may add 20 or more points to your score.

Lowering your debt-to-income ratio takes longer but has big impact. Make extra payments on high-interest credit cards or any debt with a large monthly minimum. Even retiring one small balance can drop your DTI by a point or two. Don’t open new credit accounts or take on new loans while you’re getting ready to apply. New debt raises your DTI and adds a hard inquiry to your report. If your income is low relative to your debts, look for ways to document additional earnings—pick up extra shifts, formalize a side gig, or ask for a raise. Lenders count side income as long as you can prove it’s been steady for at least six months.

Clean up your credit behavior in the months before you apply. Don’t close old credit cards unless they charge an annual fee you can’t afford. Closing accounts shortens your average account age and can hurt your score. Use prequalification tools from multiple lenders to compare soft-pull offers without triggering hard inquiries. When you’re ready to apply, gather all your documents first—pay stubs, tax returns, ID, bank statements—so you can submit everything at once and avoid delays.

Six practical strategies to improve your approval odds:

- Pay down credit card balances to reduce utilization below 30 percent, ideally below 10 percent.

- Set up automatic payments or calendar reminders to ensure every bill is paid on time for at least three to six months before applying.

- Dispute any errors on your credit reports with Equifax, Experian, and TransUnion.

- Don’t apply for new credit cards or loans in the 90 days before your consolidation application.

- Increase documented income by formalizing side work, reporting freelance earnings on your taxes, or negotiating more hours at your current job.

- Lower your DTI by making extra payments on existing debts or consolidating smaller high-interest balances with a balance-transfer card before applying for the larger loan.

Common Reasons Applicants Don’t Qualify for a Debt Consolidation Loan

Denials usually boil down to a handful of issues. Low credit score is the simplest: if your score falls below the lender’s minimum, the system flags your application before underwriting even starts. High debt-to-income ratio is the second most common block. When your monthly debt payments already eat up 45 or 50 percent of your income, lenders worry you won’t have enough left to reliably cover a new loan payment. Unstable or insufficient income also triggers denials, especially if you’ve changed jobs a lot, have employment gaps, or can’t document consistent earnings.

Recent problems or serious negative marks—late payments in the past six to twelve months, accounts in collections, charge-offs, or a bankruptcy within the past few years—make lenders nervous. Even if your score has bounced back somewhat, recent missed payments signal elevated risk. Some lenders have hard rules: no bankruptcies within seven years, no accounts in collections, no more than one late payment in the past year. Trip any of those wires and approval becomes unlikely until time passes and those marks age off your report or you settle outstanding accounts.

Five common reasons for denial:

- Credit score below the lender’s minimum threshold

- Debt-to-income ratio exceeding 40 to 45 percent

- Unverified or unstable income (job changes, gaps, or inconsistent deposits)

- Recent late payments, collections, charge-offs, or bankruptcy

- Requested loan amount too high relative to income and existing debt load

If you’re denied, ask the lender why. Many send an adverse-action notice listing the factors. Use that feedback to fix weak spots—pay down debt, wait for negative marks to age, boost income documentation—and reapply in three to six months. Some borrowers also try applying for a smaller loan amount or adding a creditworthy cosigner to improve approval chances next time.

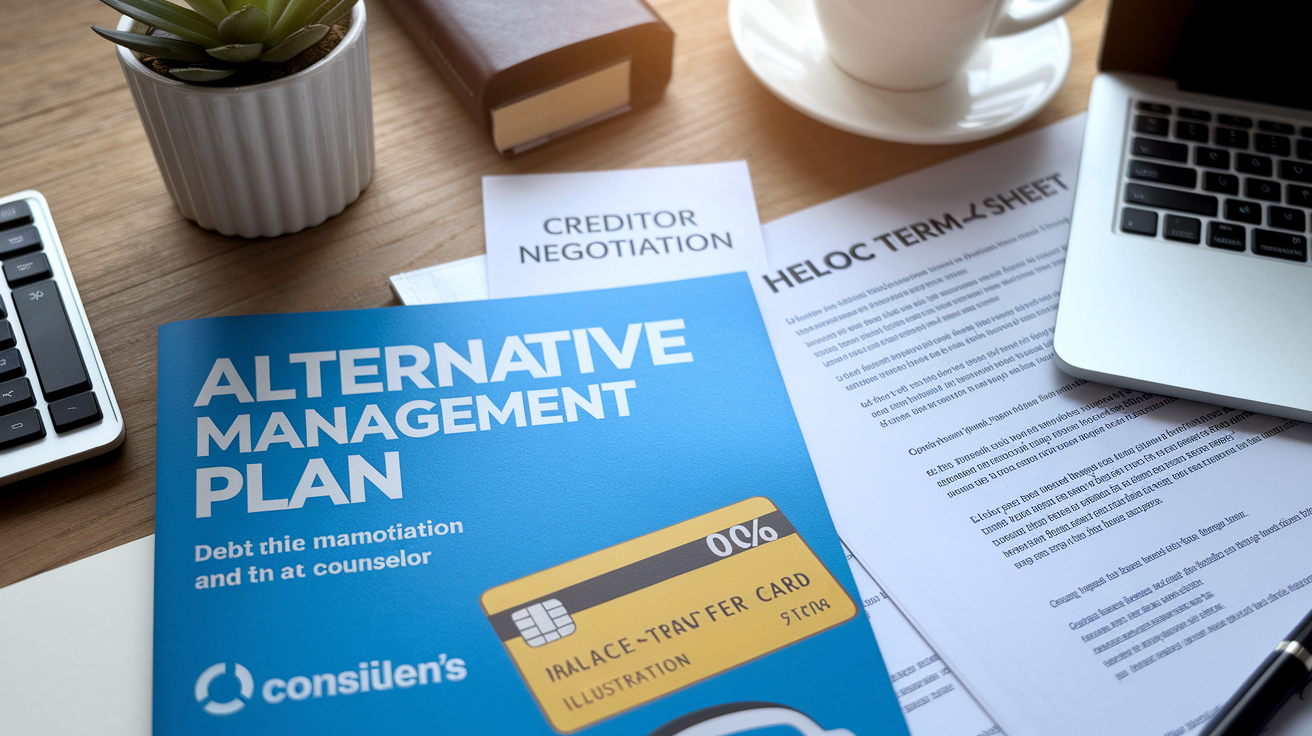

Alternatives if You Can’t Qualify for a Debt Consolidation Loan

When a traditional consolidation loan isn’t available, you still have ways to simplify payments and cut interest. A debt management plan through a nonprofit credit-counseling agency consolidates your unsecured debts into one monthly payment without requiring a new loan. The counselor negotiates with your creditors to lower interest rates—often into single digits—and waives certain fees. You make one payment to the agency and they distribute it to your creditors. DMPs don’t require a high credit score, but you do have to close the enrolled credit card accounts and commit to a multi-year repayment plan, typically three to five years.

Balance-transfer credit cards with 0 percent introductory APR periods offer another path if your credit is fair to good. You transfer existing credit card balances to the new card and pay no interest for 12 to 21 months. The catch is a balance-transfer fee, usually 3 to 5 percent of the amount transferred, and you need to pay off the full balance before the promo period ends or the rate jumps to the card’s standard APR, often 18 percent or higher. This works best if you can commit to aggressive monthly payments and clear the debt within the intro window.

If you own a home and have equity, a HELOC can work even if you don’t qualify for an unsecured loan. Rates are typically lower because your home secures the debt, but that also means foreclosure risk if you default. Qualification depends on your equity, credit score (usually 620 or higher), and income, not just your unsecured credit profile. You can also try negotiating directly with creditors—explain your situation, ask for a lower interest rate or hardship payment plan, and request fee waivers. Some creditors will work with you, especially if the alternative is you falling further behind or filing bankruptcy.

| Alternative | Key Requirement | Risk/Trade-Off |

|---|---|---|

| Debt Management Plan (DMP) | Commitment to close enrolled credit cards; work with nonprofit counselor | Takes 3–5 years; limits access to new credit during plan |

| 0% Balance-Transfer Card | Fair to good credit; ability to pay off balance within intro period | 3–5% transfer fee; high APR after promo ends if balance remains |

| HELOC (Home Equity Line) | Home ownership, sufficient equity, credit score ~620+ | Home at risk if you default; variable interest rate can increase payments |

| Creditor Negotiation | Willingness to call and negotiate; proof of hardship helps | Not guaranteed; may result in closed accounts or credit-report notes |

Final Words

in the action you learned the key checks lenders make: credit score, debt-to-income ratio, steady income and employment, plus paperwork like pay stubs and tax returns.

If your score is near 650 and DTI is under 40%, try a soft prequalification to see offers. If not, focus on small wins: pay down balances, fix report errors, or document extra income.

Do one thing this week—check your score or pull recent pay stubs. That simple move starts the path to how to qualify for debt consolidation loan and a lower monthly payment.

FAQ

Q: Is it hard to get approved for debt consolidation?

A: Getting approved for debt consolidation depends on your credit score, debt-to-income ratio (DTI), income, and job history. Lenders commonly want about a 650+ score and DTI under 40%; consider secured options or counseling if not.

Q: How much is the payment on a $50,000 consolidation loan?

A: The payment on a $50,000 consolidation loan depends on APR and term. For example, at 10% over 5 years it’s about $1,063/month; at 7% over 7 years it’s about $755/month. Longer terms lower payments.

Q: What qualifies you for a debt consolidation loan?

A: What qualifies you for a debt consolidation loan is a usable credit score, manageable DTI, steady income, and documentation. Typical thresholds: roughly a 650 minimum score, DTI below 40%, and about two years’ steady employment.

Q: What credit score do you need to get a $30,000 loan?

A: The credit score you need to get a $30,000 loan is commonly about 650 or higher for unsecured loans; higher scores earn lower APRs. Lenders also consider income and DTI, so prequalify to see your rate.