{kind=link}

What if overspending wasn’t a failure of will, but a missing tool?

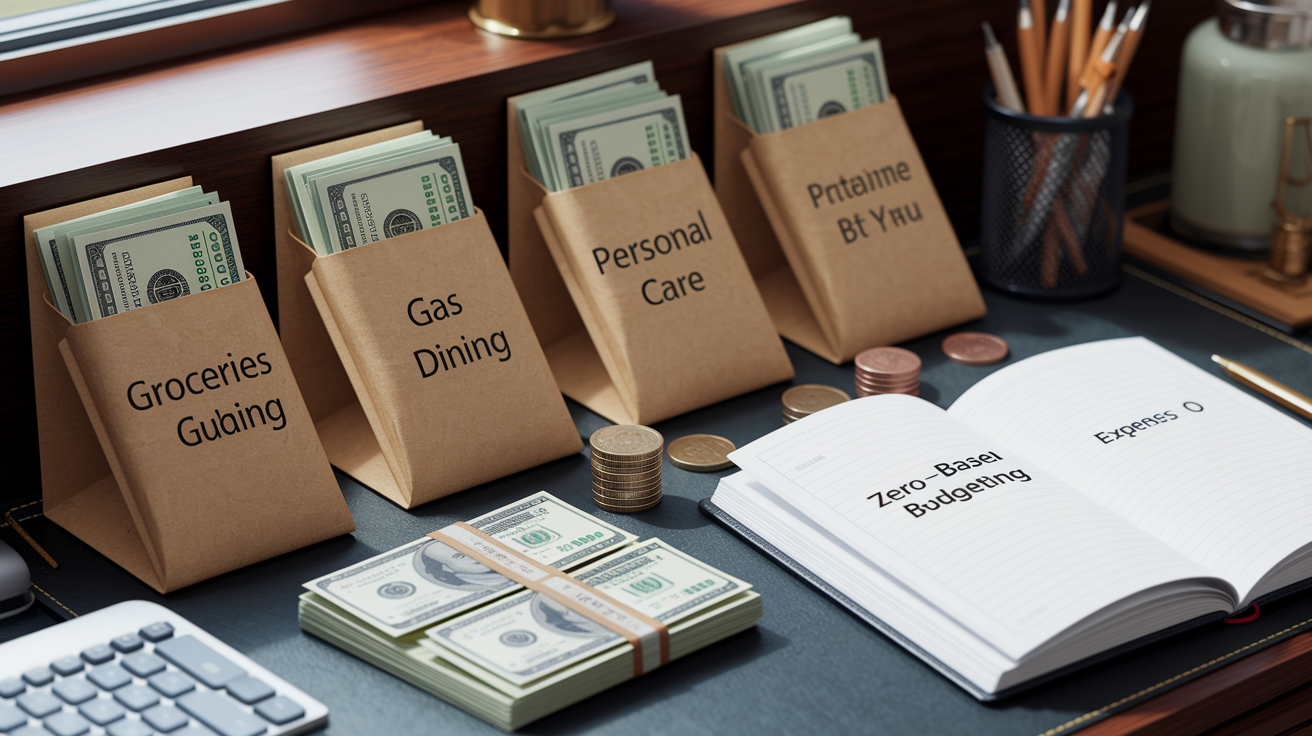

The envelope budgeting system makes money visible: you divide your paycheck into labeled envelopes and spend only what’s inside.

It’s a low-tech way to force better choices, stop impulse buys, and actually save.

In this article you’ll learn how to set it up, which categories to use, and what to do when an envelope runs dry.

If you regularly blow grocery or dining-out budgets, start with 6 to 10 envelopes and watch your month change.

How the Envelope Budgeting System Works in Practical Terms

The envelope budgeting system (sometimes called “cash stuffing”) is a physical, cash-based method where you divide your monthly income into labeled envelopes that represent specific spending categories. Each envelope holds only the amount of money you’ve budgeted for that category. The core rule is simple: when the envelope’s empty, you stop spending in that category for the rest of the month.

This method connects directly to zero-based budgeting, where every dollar of income gets assigned a job before the month begins. Income minus all assigned expenses should equal zero. Instead of tracking numbers in a spreadsheet, you can see and touch your remaining budget. When you hand over cash at the register, the physical act of watching bills leave your wallet makes spending feel more real than swiping a card.

The behavioral mechanism is visibility. You can glance at an envelope and instantly know how much is left. If your dining out envelope’s nearly empty on the 15th, you know you need to cook at home for the rest of the month. That immediate feedback loop helps you make better spending decisions in the moment.

Common envelope categories include:

- Groceries

- Gas or transportation

- Restaurants and dining out

- Hair care and personal grooming

- Fun money or entertainment

- Car maintenance and repairs

The system works because it turns abstract budget numbers into a concrete, visible constraint. You’re not guessing whether you can afford something. You’re checking whether the envelope still has cash in it.

Budgeting Setup and Envelope Categories for the Cash Envelope Method

Start by separating your expenses into two groups: fixed and variable. Fixed expenses stay the same every month (mortgage or rent, insurance premiums, utilities, subscription services). Variable expenses change month to month based on your choices and behavior (groceries, gas, dining out, entertainment, clothing).

Most people keep fixed expenses on autopay or write checks, then use physical envelopes only for the variable categories where they tend to overspend. If you consistently blow your grocery budget or spend too much eating out, those are the categories that benefit most from a physical envelope.

When creating categories, follow these selection rules:

- Avoid broad labels like “miscellaneous.” Break them into specific purposes such as car repairs, cash donations, or pet care.

- Start with 6 to 10 envelopes. Too many categories make the system hard to track.

- Focus on the categories where you lose control or regularly go over budget.

- Include at least one envelope for irregular but predictable costs, like annual insurance or holiday gifts.

- Create a dedicated envelope for savings or debt repayment and treat it as a required expense, not leftover money.

You don’t need an envelope for every line item in your life. The envelope system is a tool for discipline in the areas where you need it most. If you never overspend on gas, you can track that expense digitally or just fill up the tank when needed. Save the envelopes for the categories that trip you up.

Step-by-Step Instructions for Setting Up Envelope Budgeting

Setting up envelope budgeting takes about an hour the first time, then becomes a quick monthly routine once you know your numbers and categories.

Calculate Monthly Income

Start with your monthly net income (the amount that actually hits your bank account after taxes and deductions). If you’re paid twice a month, add both paychecks. If your income fluctuates, use the lowest consistent monthly amount from the past three to six months so you don’t overcommit.

Include all regular income sources: wages, Social Security, pension payments, side gig income. If you receive irregular bonuses or seasonal income, don’t count those in your baseline monthly total. Treat windfalls separately when they arrive.

Create and Label Categories

Write each spending category on a separate envelope. Include the category name and the budgeted dollar amount. For example, “Groceries – $400” or “Gas – $150.” Use clear, specific labels instead of vague terms.

Don’t create a catch all “miscellaneous” envelope. If you regularly spend on something, it deserves its own envelope. Car repairs, donations, clothing, personal care. Each gets a dedicated envelope so you can see patterns over time.

Allocate Cash and Fund Envelopes

Once categories are labeled, assign a dollar amount to each envelope so the total equals your monthly income. If you earn $3,000 per month, your envelope totals must add up to exactly $3,000. Zero-based budgeting in action.

Withdraw the cash you need from your bank or ATM and divide it into the envelopes. If you budget $700 for groceries and get paid twice a month, withdraw $350 from each paycheck and add $350 plus $350 to the “Groceries” envelope. Split larger amounts across paychecks to avoid carrying too much cash at once.

Spend Only From Envelopes

When you go to the grocery store, bring the grocery envelope. Pay with the cash inside and put your change back into the same envelope. If you forget the envelope at home, go back and get it rather than using your debit card or another envelope’s cash.

If you spend most of an envelope early in the month, cut back for the rest of the cycle. Meal plan from what’s in the pantry, shop sales, use coupons, or skip a trip. The physical limit forces you to adjust behavior instead of swiping a card and hoping it works out.

What Happens When Envelope Funds Run Out

When an envelope’s empty, you stop spending in that category. That’s the rule. If your restaurant envelope runs out on the 18th, you eat at home for the rest of the month. The shortage is a signal to adjust your habits, not an invitation to raid another envelope.

Borrowing from other envelopes defeats the purpose. If you pull money from your gas envelope to cover another restaurant meal, you’ll run short on gas later and create a cascade of problems. Treat each envelope as a firm boundary.

If you face an empty envelope, your approved options are:

- Stop spending in that category until next month.

- Formally reallocate money from a lower priority envelope and record the change in writing.

- Adjust future months’ allocations if the pattern repeats, but don’t change mid-month on impulse.

- For true emergencies, involve a spouse or accountability partner in the decision to reallocate, then adjust your budget immediately.

Running out isn’t a failure. It’s feedback. If your grocery envelope empties every month by the 20th, you need to either increase the grocery allocation or reduce portion sizes, shop sales harder, or cut restaurant spending to free up cash. The system gives you data. Your job is to respond.

Handling Leftover Cash in the Envelope Budgeting System

If you reach the end of the month and cash remains in an envelope, you have a few good options. Don’t treat leftover money as “bonus” spending money. Use it strategically to build financial stability.

The best use depends on where you are in your financial journey. If you don’t have a starter emergency fund, apply leftover cash there until you reach $1,000. That small buffer keeps you from raiding envelopes or going into debt when an unexpected expense hits.

If your emergency fund’s in place and you’re working on debt, add leftover envelope cash to your debt snowball. Pay extra on your smallest debt to accelerate payoff, then roll that payment into the next debt once the first is gone.

Recommended uses for leftover funds:

- Build or top off your starter emergency fund (target $1,000).

- Make an extra payment on your smallest debt (debt snowball method).

- Start a sinking fund for irregular expenses like car insurance, holiday gifts, or home repairs.

If a specific category consistently has money left over, adjust next month’s allocation downward and redirect that cash to a higher priority envelope or goal. Patterns tell you where your budget estimates are off.

Physical Cash Envelopes vs. Digital Envelope Alternatives

The traditional envelope budgeting system uses physical cash and paper envelopes. That’s where the behavioral power comes from. Handing over real bills makes spending feel tangible. Digital alternatives exist, but they don’t replicate the same psychological impact.

| Method | Advantages | Limitations |

|---|---|---|

| Physical cash envelopes | Immediate visibility, strong behavioral change, no technology required, works offline | Requires cash withdrawals, inconvenient for online purchases, risk of loss or theft, no transaction rewards |

| Bank sub-accounts | Organized digital tracking, safer than cash, easier for bill payments, integrates with direct deposit | Weaker psychological friction, easy to transfer between accounts, less visible spending limits |

| Budgeting apps (Goodbudget, YNAB, EveryDollar) | Convenient, tracks online and card purchases automatically, generates reports, syncs across devices | Requires consistent manual entry or syncing, no physical spending barrier, monthly subscription costs for some apps |

You can use a hybrid approach: physical cash envelopes for high risk categories like dining out and entertainment, while tracking fixed expenses and online purchases in a budgeting app. For online shopping, write the budgeted amount on the envelope and record each purchase on the back. When the written total reaches the budgeted amount, stop buying online in that category just as you would if the cash were gone.

Apps like Goodbudget let you set up virtual envelopes and track spending, but you’re still using a debit or credit card. The act of swiping doesn’t create the same pause that counting out bills does. If you’ve never overspent with cards, a digital system might work fine. If cards are part of your overspending problem, stick with physical cash.

Example of Envelope Budgeting Using Real Numbers

Here’s a realistic monthly budget for someone earning $3,000 net per month. Every dollar is assigned to an envelope so income minus expenses equals zero (the foundation of zero-based budgeting).

Each category gets a fixed allocation. If an expense is lower one month, the leftover cash stays in the envelope or moves to savings. If a category runs over, you must cut spending in another envelope to stay on track.

| Category | Amount |

|---|---|

| Rent | $1,200 |

| Utilities | $200 |

| Groceries | $400 |

| Transportation (gas, parking) | $250 |

| Insurance | $150 |

| Savings | $300 |

| Dining & entertainment | $250 |

| Miscellaneous (personal care, clothing) | $250 |

Let’s say you overspend in groceries by $50 mid-month because you hosted an unexpected dinner. You have two choices: cut $50 from dining and entertainment for the rest of the month, or reduce miscellaneous spending by $50. You can’t simply add $50 to the grocery envelope without taking it from somewhere else. The system forces trade-offs in real time, which builds decision making discipline and prevents the “I’ll figure it out later” mindset that leads to overspending.

Pros and Cons of the Envelope Budgeting Method

The envelope system isn’t for everyone. It has clear strengths and real limitations, and your decision to use it should match your spending habits and lifestyle.

Pros:

- Creates immediate accountability. You can see what’s left at a glance.

- Reduces overspending by enforcing a hard physical limit on each category.

- Builds discipline through repetition and visible consequences.

- Works without technology, apps, or internet access.

- Effective for people who overspend when using credit or debit cards.

Cons:

- Requires regular trips to withdraw and manage physical cash.

- Time consuming to organize, label, and track envelopes manually.

- Inconvenient for online purchases or automatic bill payments.

- Provides no credit card rewards, cash back, or purchase protection.

- Risk of losing cash if envelopes are misplaced or stolen.

If you’re rebuilding spending habits after a period of overspending, the friction and visibility of physical cash can be exactly what you need. If you have stable self-control and prefer digital convenience, the system may feel unnecessarily restrictive. Match the tool to the problem you’re solving.

Tips for Successful Budgeting With the Envelope System

Success with envelope budgeting comes from consistent habits and honest adjustments. The system only works if you follow the rules every month and respond to the data it gives you.

- Track online purchases by writing each amount on the back of the corresponding envelope. Treat digital spending the same as cash spending and stop when the written total reaches the budgeted amount.

- Plan meals and shop with a list to stretch your grocery envelope further. Use sales, coupons, and pantry staples when funds run low.

- Avoid mixing card and cash spending in the same category. Pick one method per envelope and stick with it for a full month before evaluating.

- Involve your spouse or accountability partner in reallocation decisions so you don’t quietly borrow from envelopes without discussion.

- Review your envelopes at month end and adjust allocations after one to three cycles if patterns show consistent overspending or underspending.

- Start with a small number of envelopes (six to eight) for your highest risk categories, then expand only if needed.

The envelope system turns budgeting into a visible, daily practice. Over time, checking your envelope balance before spending becomes automatic. You stop asking “Can I afford this?” and start asking “Is there cash in the envelope?” That small mental shift builds long-term spending awareness and reduces impulse purchases even after you move to other budgeting methods.

Final Words

In practice, the envelope system is simple: physical cash, visible limits, and the rule that when an envelope is empty you stop spending. That alone cuts impulse buys.

We explained what it is, gave examples like groceries, gas, and restaurants, and showed how it ties to zero-based budgeting and handling leftovers. Visible limits change behavior.

If you only do one thing, try a short test with a few envelopes this month. This will show envelope budgeting system how it works and usually means steadier spending and less stress.

FAQ

Q: How does envelope budgeting work simple?

A: The envelope budgeting method works simply by using physical cash envelopes for each spending category and only spending what’s inside. When an envelope is empty, you stop spending in that category until it’s refilled.

Q: How much money does the $100 envelope save and does the 100 envelope challenge actually work?

A: The $100 envelope challenge saves whatever you deposit — $100 per week or month — so 12 deposits give $1,200. It works if you stick to it and don’t borrow from other envelopes.

Q: What is the 70/20/10 rule money?

A: The 70/20/10 rule for money is a simple split: 70% for needs, 20% for savings or debt payments, and 10% for wants. Use it as a baseline and adjust for your goals.